Hello Stéphane,

Thanks for the responses. I am stuck so these are very helpful. Sorry for being vague about my description before.

- The package I was referring to is

“Solving Dynamic General Equilibrium Models Using a Second-Order Approximation to the Policy Function,” by Stephanie Schmitt-Grohe and Martin Uribe (JEDC, vol. 28, January 2004, pp. 755-775)

They use symbolic toolbox to calculate the derivatives and once you provide the system a point (whether it is steady state or not) it calculates the impulse responses and second moments etc…

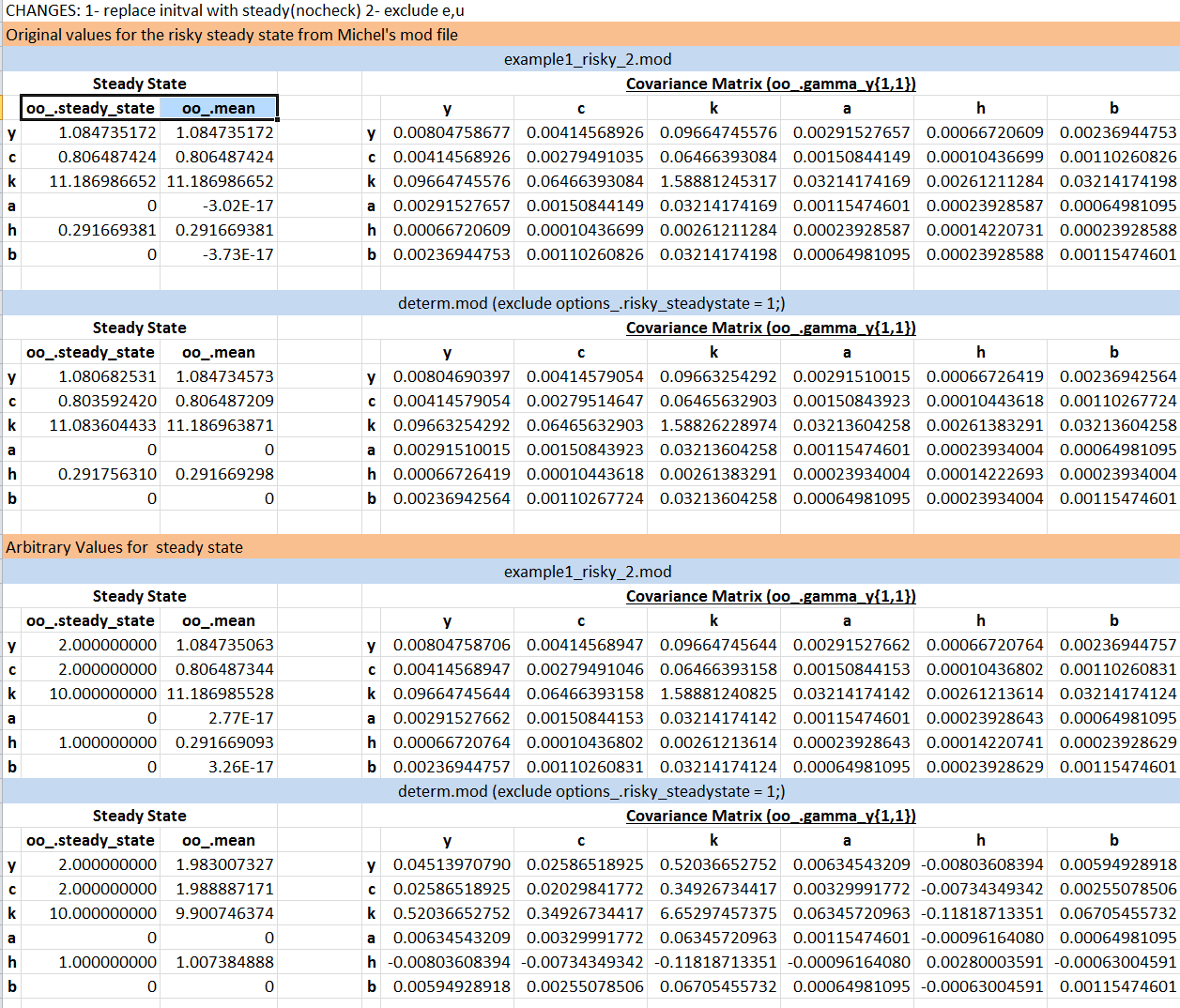

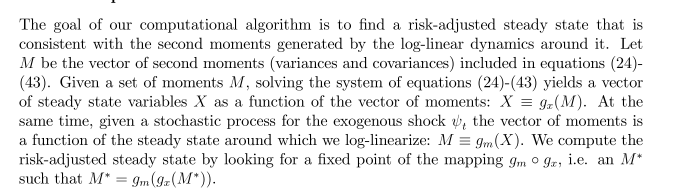

- The risky steady state I am referring to is not widely used but the main idea is as

Gertler, Mark, Nobuhiro Kiyotaki, and Albert Queralto. “Financial crises, bank risk exposure and government financial policy.” Journal of Monetary Economics 59 (2012): S17-S34.

Similar method is applied also by

de Groot, Oliver. “Computing the risky steady state of DSGE models.” Economics Letters 120.3 (2013): 566-569.

The basic idea is to find the risky steady state by iterating on moments until they converge. But all these papers I think use the SGU package and i am trying to do this in dynare

- Thanks to your suggestions, i was able to resolve the issue of Dynare stopping if it does not have a completely accurate steady state.

I have an external steady state file that computes the steady state and in deterministic setting with steady_state_block i get residiuals in all equations 0. Also with initval letting dynare to find the steady state it still works

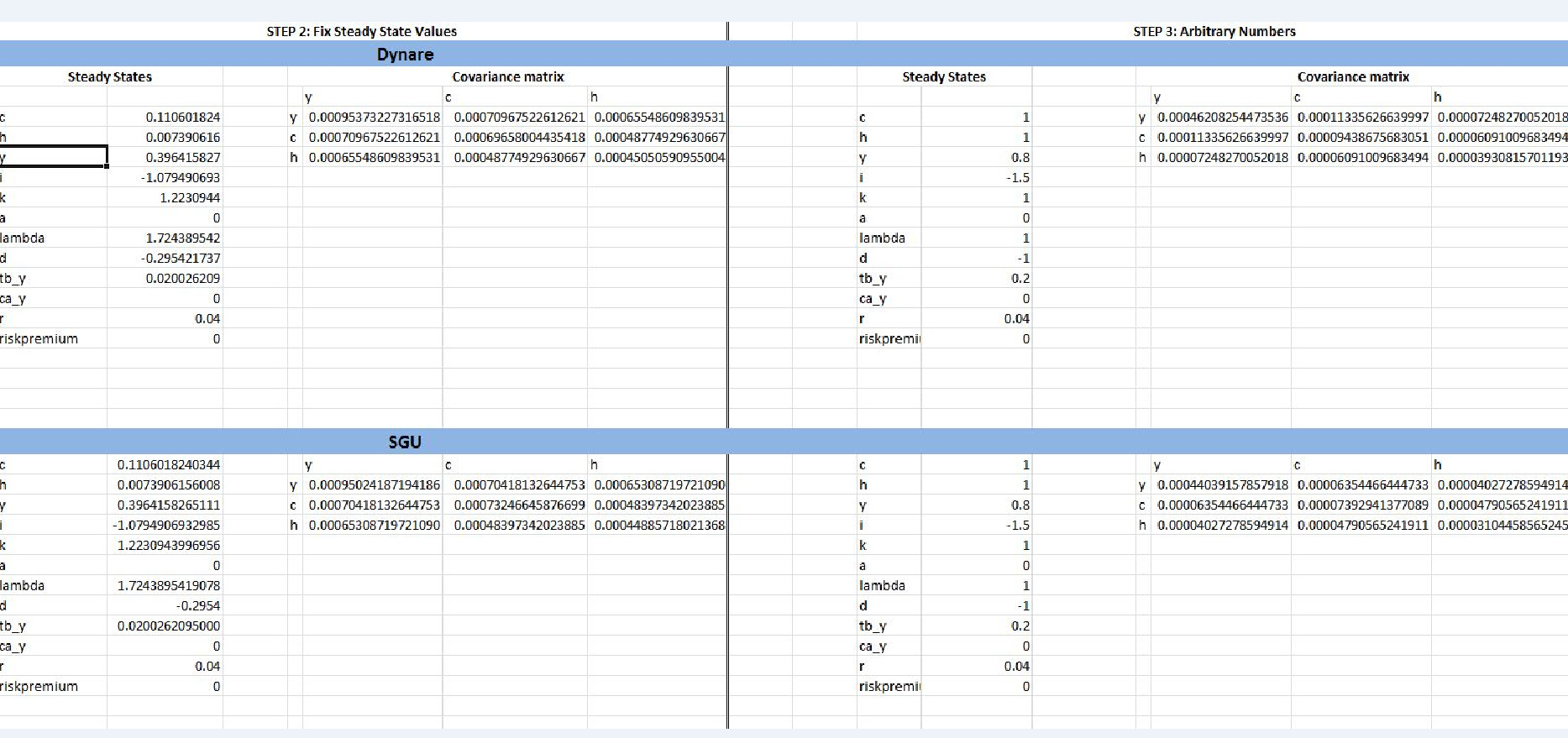

- But after working on this a bit, I do not think dynare calculates the covariance function (or at least updates it) with steady(nocheck) option

I mean after two iterations, even though my external steady state file produces different steady states as i update them with second moments, the oo_.gamma_y{1,1} matrix remains the same after the second iteration. It is not updated.

I do get small errors in residuals but that is ok, my point is to be constantly receiving an new covariance matrix for each new steady state i provide.

You mentioned that dynare uses a nonlinear solver. Does this mean that even if I provide dynare a steady state (without focusing on whether residuals of equations are all 0s) and want it to give me the results at that point given by my external file, dynare will ignore this and will use its own nonlinear solver?

In other words, lets assume steady state of a variable is 5. But my external file gives the initial value for this as 4.8, will dynare with steady(nocheck) option provide me with a covariance matrix around 4.8 or will it use its solver and go to 5 and give me the oo_.gamma_y{1,1}. I want to get oo_.gamma_y{1,1} at 4.8. That is what confuses me

Appreciate your help very much. Just with package programs like dynare many things become so much simpler but certain things remain a black box and i am not that good in going into details of the dynare code, that is why i wanted to ask

PS: In the code, i just changed the steady state value of a variable in steady_state_block to be 10000. I get huge errors in residual function but the oo_.gamma_y{1,1} stays the same

PS2: Is it possible in dynare to completely shut its steady state calculation. Something similar to set_param_value(‘alpha_K’,P.alpha_K ); and setting steady state value of a variable lets say K to be 1000 and not having dynare change this value

Best regards