Dear all,

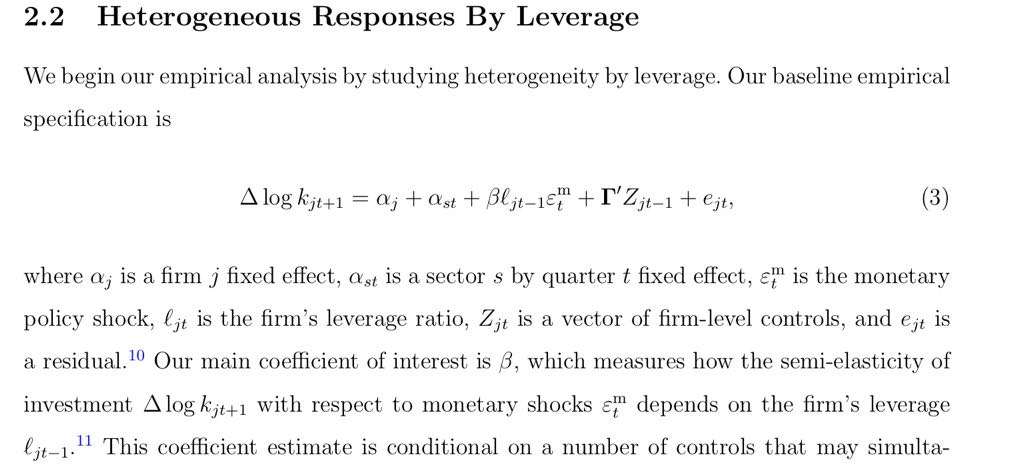

I have a question relating to fixed effect. I have encounter it many times in quantitative macro paper. For example, like in the following picture from a paper by Ottonello & Winberry.

As you can see, in the regression equation, they put two constant terms \alpha_j and \alpha_{st}, saying that which are firm and sector fixed effects respectivily.

So I am a bit confused, are they indeed dummy variables, for example \alpha_j will be 1 for firm j and 0 otherwise? I mean the dummy variables which are often used to kill fixed effects?

Is there anyone having an idea? Really appreciate!

Thank you,