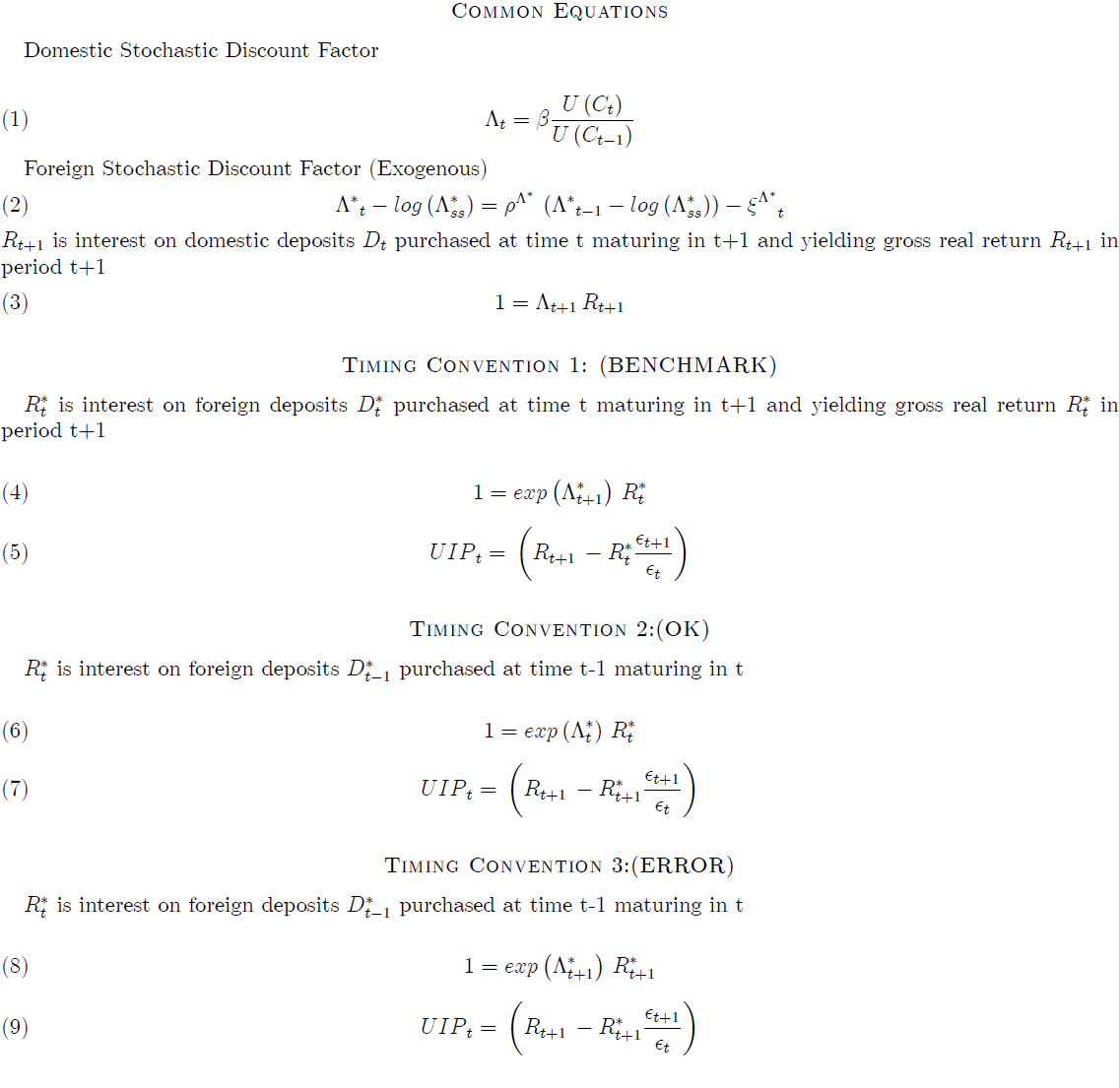

Dear all,

I am a bit confused with the dynare timing convention. I UIP deviation of returns on domestic and foreign deposits. Domestic deposits Dt-1 purchased at t-1 yield Rt at time t. Domestic stoch. discount factor comes from euler eqn. Foreign stoch, discount factor follows exogenous process.

I have three timing conventions for foreign return. My confusions are

-

List item: Timing conventions 1 and 2 work fine in first order approximation but in second order approximation i have different correlation, variance decomposition matrices

-

List item Timing convention 3 does not work. I get the error message that Blanchard Kahn conditions are not satisfied. I am wondering why that is the case as it seems to me that case 3 and case 2 are identical

I have prepared the image below to summarize the issues. Any help would be appreciated.

Thanks