I am new to dynare and therefore my question may be to straightforward:

I want to simulate a negative technology news shock in the classical DSGE-model which happens after 4 periods. I belive, this shock will lead to a drop of the natural interest rate. That is my ultimate goal at the end of the simulation.

What do I need to change if I use the exact Gali 2008 model: https://github.com/JohannesPfeifer/DSGE_mod/blob/master/Gali_2008/Gali_2008_chapter_3.mod

Which equations and which definitions have to be replaced or added to the model?

I implemented the shock and it worked as it should. The thing is, I hoped the natural interest rate would sink, when implementing the technology news shock. Unfortunatly, it sinks for as long as the shock is only anticipated, but when it happens, the natural interest rate goes up again. What do I need to alter in the model and in the code to make the natural interest rate stay at a level below zero for some periods longer,even better for a long time?

Thank you so much!

You need to think about the intuition behind the IRFs. An anticipated technology shock means that it makes sense to not work today when technology is low. That means equilibrium labor should be low today and high in the future (substitution effect). At the same time, there should be an income effect: agents consume more of the consumption good and of leisure. However, we know that once TFP goes up, consumption will jump up. That means the consumption path is increasing. The Euler equations then requires a higher interest rate (above the rate of time preference). Those effects should determine the movement of the interest rate in the flex-price economy.

Thank you for your answer!

does this mean, that the natural interest rate will be only low while the individuals expect the technology to drop? Would an additional expansionary monatary policy shock (simultainously with the negative technology news shock) keep the natural interest rate down? I belive, expansionary monatary policy should enhance the effect of a low natural interest rate even after the actual negative technology shock has taken place. How do I combine this shocks in dynare for them to happen at the same time?

Thanks again!

It’s not my model so I have no idea what is going on in your model. I only pointed out that you should think hard about the economics of the problem and provided you with my understanding of what would happen after a positive news shock about TFP in an RBC model .

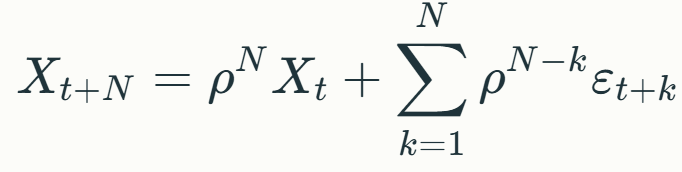

Again for analytical understanding, for a stationary AR(1) process, iterated forward N periods, would it be correct to understand that the second part of the RHS would capture news shocks known at t, while the first term would capture the surprise shock?

Your timing here looks strange. What does the time index represent? The news shock literature typically employs it to indicate the information set. In that case, it would be something more like

X_t+n=…+\varepsilon_{t-k}

because the shock was already known k periods in the past but it only affects the variable now.

Thank you for your reply @jpfeifer, and apologies, I didn’t state my question and notation very clearly earlier. I’ll give it a go again:

Consider a stationary AR(1) process, X_t = \rho X_{t-1} + \varepsilon_{t-k} for k \geq 0

where k=0 would be a surprise shock and k>0 would be a news shock.

If we iterate it forward N periods, we would get:

X_{t+N} = \rho^N X_t + \sum_{j=1}^{k-1} \rho^{N-j} \varepsilon_{t + j - k} for k \geq 1, where we assume the surprise shock at k=0 is already embedded in the current state to prevent double counting.

I’m interested in Y_t = E_t [X_{t+N}-X_t] to see how surprise and news shocks in X affect Y_t.

impact of a news shock known at t, but to be realised after t, would be E_t[\rho^{N-j} \varepsilon_{t + j - k}]=\rho^{N-j}\varepsilon_{t + j - k} as these are known values

and impact of news shocks realised at or before t would be (\rho^N-1)X_t as it is already included in current state X_t?