Hi all,

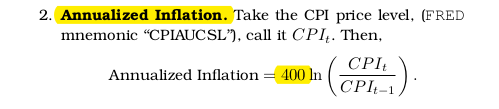

I am here from Edward P. Herbst and Frank Schorfheide (Bayesian Estimation

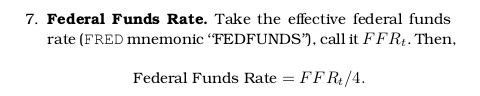

of DSGE Models). I am not sure why the author uses two different specifications for the federal funds rates for two quarterly frequency models.

In one model, he uses this:

And in the other model, it is the following:

"FEDFUNDS" is monthly data on FRED website, and since the author says just 'call it FFR_t’ per the instruction, I am kinda confused about the frequency of t in FFR_t per the instruction. I will appreciate it if someone understand these instructions in the book and can clarify a little bit…

Same problem with inflation where ‘‘CPIAUCSL’’ is monthly data, and the instruction says: