i am novice.i need help from the seniors to run this mod.

welfare.xlsx (12.8 KB)

welfare2018.mod (11.0 KB)

i am novice.i need help from the seniors to run this mod.

welfare.xlsx (12.8 KB)

welfare2018.mod (11.0 KB)

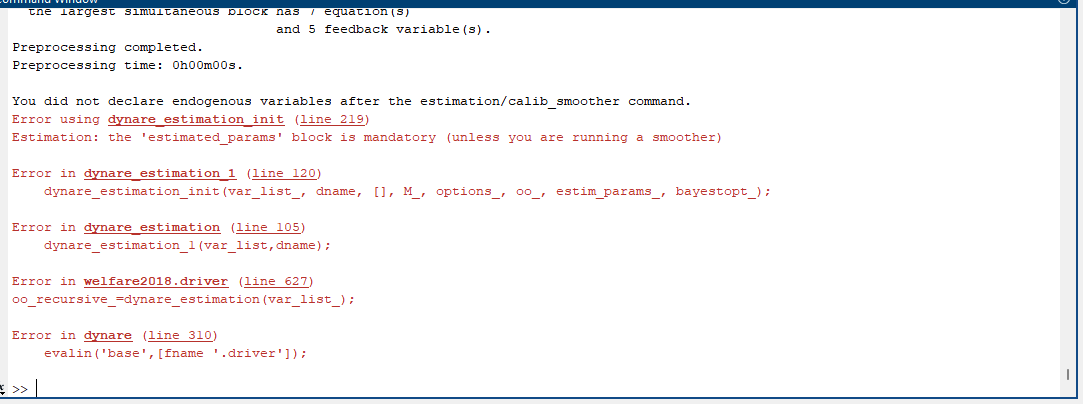

What is the problem exactly when you run this model ?

You did not declare estimated_params block in your mod file.

This block is mandatory when you estimate a DSGE model in dynare.

/*

/*

@#ifndef fixed_WPC_slope

@#define fixed_WPC_slope=0

@#endif

@#ifndef SGU_framework

@#define SGU_framework=0

@#endif

@#ifndef Calvo

@#define Calvo=1

@#endif

@#ifndef taxes

@#define taxes=0

@#endif

var pi_p {\pi^p} (long_name=‘price inflation’)

y_gap {\tilde y} (long_name=‘output gap’)

y_nat {y^{nat}} (long_name=‘natural output’) //(in contrast to the textbook defined in deviation from steady state)

y {y} (long_name=‘output’)

yhat {\hat y} (long_name=‘output deviation from steady state’)

r_nat {r^{nat}} (long_name=‘natural interest rate’)

r_real {r^r} (long_name=‘real interest rate’)

i {i} (long_name=‘nominal interrst rate’)

n {n} (long_name=‘hours worked’)

m_real {(m-p)} (long_name=‘real money stock’)

m_growth_ann {\Delta m} (long_name=‘money growth annualized’)

m_nominal {m} (long_name=‘nominal money stock’)

nu {\nu} (long_name=‘AR(1) monetary policy shock process’)

a {a} (long_name=‘AR(1) technology shock process’)

r_real_ann {r^{r,ann}} (long_name=‘annualized real interest rate’)

i_ann {i^{ann}} (long_name=‘annualized nominal interest rate’)

r_nat_ann {r^{nat,ann}} (long_name=‘annualized natural interest rate’)

pi_p_ann {\pi^{p,ann}} (long_name=‘annualized inflation rate’)

z {z} (long_name=‘AR(1) preference shock process’)

p {p} (long_name=‘price level’)

w {w} (long_name=‘nominal wage’)

c {c} (long_name=‘consumption’)

w_real \omega (long_name=‘real wage’)

w_gap {\tilde \omega} (long_name=‘real wage gap’)

pi_w {\pi^w} (long_name=‘wage inflation’)

w_nat {w^{nat}} (long_name=‘natural real wage’)

mu_p {\mu^p} (long_name=‘markup’)

pi_w_ann {\pi^{w,ann}} (long_name=‘annualized wage inflation rate’)

;

varexo eps_a {\varepsilon_a} (long_name=‘technology shock’)

eps_nu {\varepsilon_\nu} (long_name=‘monetary policy shock’)

eps_z {\varepsilon_z} (long_name=‘preference shock innovation’)

;

parameters alppha {\alpha} (long_name=‘capital share’)

betta {\beta} (long_name=‘discount factor’)

rho_a {\rho_a} (long_name=‘autocorrelation technology shock’)

rho_nu {\rho_{\nu}} (long_name=‘autocorrelation monetary policy shock’)

rho_z {\rho_{z}} (long_name=‘autocorrelation demand shock’)

siggma {\sigma} (long_name=‘inverse EIS’)

varphi {\varphi} (long_name=‘inverse Frisch elasticity’)

phi_pi {\phi_{\pi}} (long_name=‘inflation feedback Taylor Rule’)

phi_y {\phi_{y}} (long_name=‘output feedback Taylor Rule’)

eta {\eta} (long_name=‘semi-elasticity of money demand’)

epsilon_p {\epsilon_p} (long_name=‘demand elasticity goods’)

theta_p {\theta_p} (long_name=‘Calvo parameter prices’)

epsilon_w {\epsilon_w} (long_name=‘demand elasticity labor services’)

@#if Calvo

theta_w {\theta_w} (long_name=‘Calvo parameter wages’)

@#else

phi_w {\phi_w} (long_name=‘Rotemberg parameter wages’)

@#endif

tau {\tau} (long_name=‘labor subsidy’)

lambda_w {\lambda_w} (long_name=‘Slope of the wage PC’)

tau_n_SS {bar {\tau^n}} (long_name=‘Steady state labor tax’)

;

%----------------------------------------------------------------

% Parametrization, p. 67 and p. 113-115

%----------------------------------------------------------------

siggma = 1;

varphi=5;

phi_pi = 1.5;

phi_y = 0.125;

theta_p=3/4;

rho_nu =0.5;

rho_z = 0.5;

rho_a = 0.9;

betta = 0.99;

eta =3.77; %footnote 11, p. 115

alppha=1/4;

epsilon_p=9;

tau=0; //1/epsilon_p;

epsilon_w=4.5;

@#if fixed_WPC_slope

lambda_w=0.03;

@#else

theta_w=3/4;

@#endif

@#if taxes

tau_n_SS=0.99;

@#else

tau_n_SS=0;

@#endif

%----------------------------------------------------------------

% First Order Conditions

%----------------------------------------------------------------

model(linear);

//Composite parameters

#Omega=(1-alppha)/(1-alppha+alpphaepsilon_p); %defined on page 166

#psi_n_ya=(1+varphi)/(siggma(1-alppha)+varphi+alppha); %defined on page 171

#psi_n_wa=(1-alpphapsi_n_ya)/(1-alppha); %defined on page 171

#lambda_p=(1-theta_p)(1-bettatheta_p)/theta_pOmega; %defined on page 166

#aleph_p=alpphalambda_p/(1-alppha); %defined on page 172

#aleph_w=lambda_w(siggma+varphi/(1-alppha)); %defined on page 172

[name=‘New Keynesian Phillips Curve eq. (18)’]

pi_p=bettapi_p(+1)+aleph_py_gap+lambda_pw_gap;

[name=‘New Keynesian Wage Phillips Curve eq. (22)’]

pi_w=bettapi_w(+1)+aleph_wy_gap-lambda_ww_gap;

[name=‘Dynamic IS Curve eq. (22)’]

y_gap=-1/siggma*(i-pi_p(+1)-r_nat)+y_gap(+1);

[name=‘Interest Rate Rule eq. (26)’]

i=phi_pipi_p+phi_yyhat+nu;

[name=‘Definition natural rate of interest eq. (24)’]

r_nat=-siggmapsi_n_ya(1-rho_a)a+(1-rho_z)z;

[name=‘Definition wage gap, eq (21)’]

w_gap=w_gap(-1)+pi_w-pi_p-(w_nat-w_nat(-1));

[name=‘Definition natural wage, eq (16)’]

w_nat=psi_n_waa;

[name=‘Definition markup’]

mu_p=-alppha/(1-alppha)y_gap-w_gap;

[name=‘Definition real wage gap, p. 171’]

w_gap=w_real-w_nat;

[name=‘Definition real interest rate’]

r_real=i-pi_p(+1);

[name=‘Definition natural output, eq. (20)’]

y_nat=psi_n_yaa;

[name=‘Definition output gap’]

y_gap=y-y_nat;

[name=‘Monetary policy shock’]

nu=rho_nunu(-1)+eps_nu;

[name=‘TFP shock’]

a=rho_aa(-1)+eps_a;

[name=‘Production function, p. 171’]

y=a+(1-alppha)n;

[name=‘Preference shock, p. 54’]

z = rho_zz(-1) - eps_z;

[name=‘Money growth (derived from eq. (4))’]

m_growth_ann=4(y-y(-1)-eta*(i-i(-1))+pi_p);

[name=‘Real money demand (eq. 4)’]

m_real=y-etai;

[name=‘Annualized nominal interest rate’]

i_ann=4i;

[name=‘Annualized real interest rate’]

r_real_ann=4r_real;

[name=‘Annualized natural interest rate’]

r_nat_ann=4r_nat;

[name=‘Annualized inflation’]

pi_p_ann=4pi_p;

[name=‘Annualized wage inflation’]

pi_w_ann=4pi_w;

[name=‘Output deviation from steady state’]

yhat=y-steady_state(y);

[name=‘Definition price level’]

pi_p=p-p(-1);

[name=‘resource constraint, eq. (12)’]

y=c;

[name=‘definition real wage’]

w_real=w-p;

[name=‘definition real wage’]

m_nominal=m_real+p;

end;

%----------------------------------------------------------------

% define shock variances

%---------------------------------------------------------------

shocks;

var eps_nu = 0.25^2; //1 standard deviation shock of 25 basis points, i.e. 1 percentage point annualized

var eps_a = 1^2; //unit shock to technology

var eps_z = 1^2; //unit shock to technology

end;

%----------------------------------------------------------------

% steady states: all 0 due to linear model

%---------------------------------------------------------------

steady_state_model;

@#if fixed_WPC_slope

%keep fixed slope of WPC and compute parameters accordingly

@#if SGU_framework

@#if Calvo

theta_w=get_Calvo_theta(lambda_w,epsilon_w,betta,varphi,1);

@#else

phi_w=(epsilon_w-1)(1-tau_n_SS)/lambda_w(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w;

@#endif

@#else

@#if Calvo

theta_w=get_Calvo_theta(lambda_w,epsilon_w,betta,varphi,0);

@#else

phi_w=(epsilon_w-1)(1-tau_n_SS)/lambda_w(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w;

@#endif

@#endif

@#else

@#if SGU_framework

%compute slope (and ) based on Calvo parameter

@#if Calvo

lambda_w=(1-theta_w)(1-bettatheta_w)/theta_w;

@#else

phi_w=(epsilon_w-1)/((1-theta_w)(1-bettatheta_w))(1-tau_n)theta_w(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w;

lambda_w=(epsilon_w-1)/phi_w(1-tau_n)(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w;

@#endif

@#else

@#if Calvo

lambda_w=(1-theta_w)(1-bettatheta_w)/(theta_w(1+epsilon_wvarphi));

@#else

phi_w=(epsilon_w-1)/((1-theta_w)(1-bettatheta_w))(1-tau_n)theta_w(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w*(1+epsilon_wvarphi);

lambda_w=(epsilon_w-1)(1-tau_n)/phi_w*(1-alppha)(epsilon_p-1)/epsilon_p/tau_s_ptau_s_w;

@#endif

@#endif

@#endif

end;

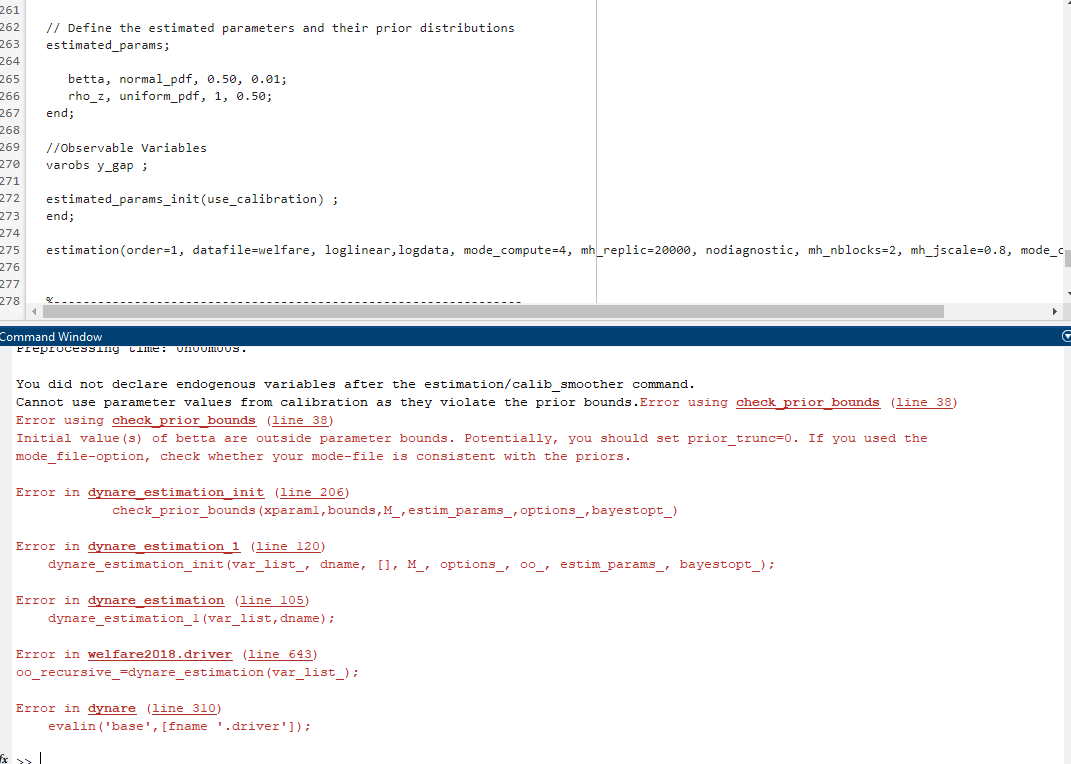

// Define the estimated parameters and their prior distributions

estimated_params;

betta, normal_pdf, 0.50, 0.01;

rho_z, uniform_pdf, 1, 0.50;

% Define other parameters to estimate…

//Observable Variables

varobs y_gap ;

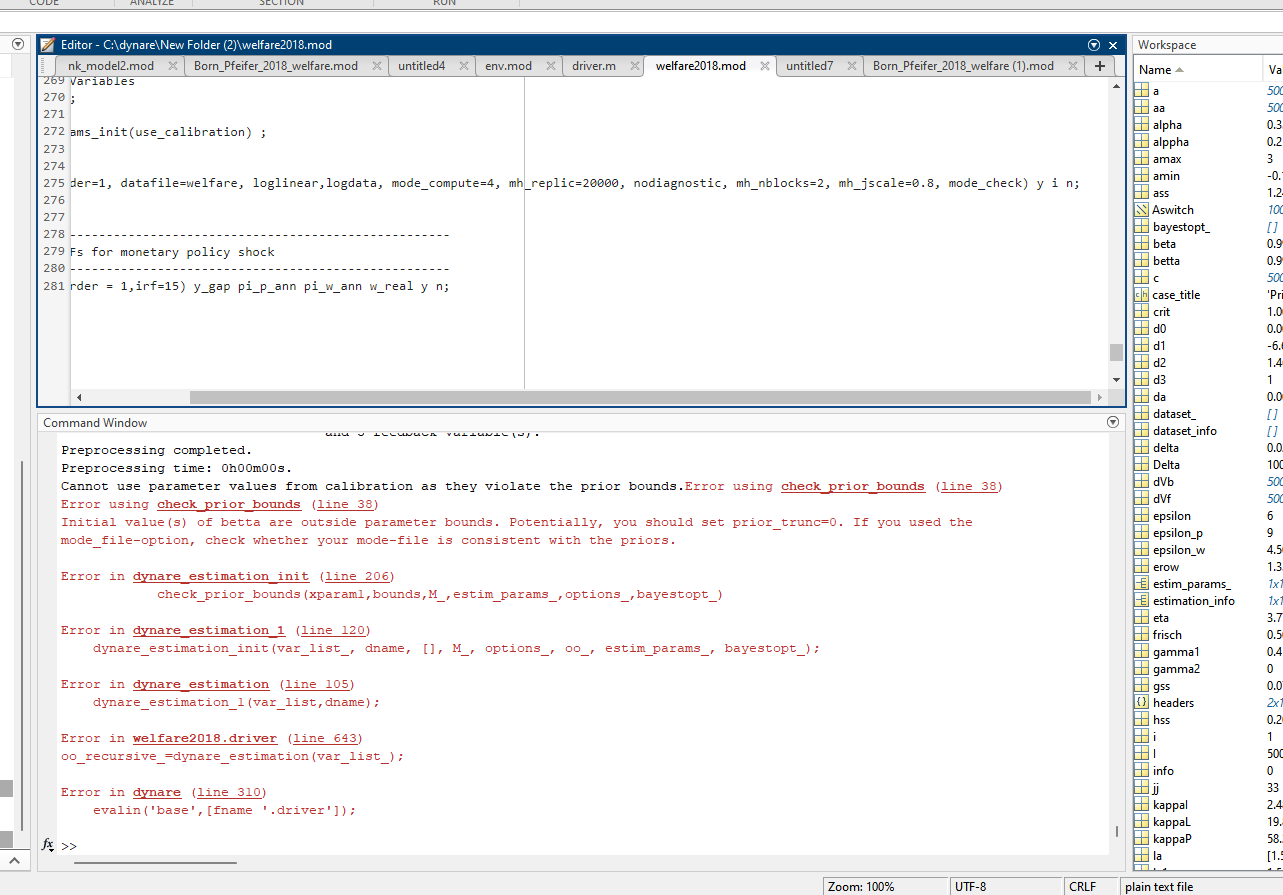

estimation(order=1, datafile=welfare, loglinear,logdata, mode_compute=4, mh_replic=20000, nodiagnostic, mh_nblocks=2, mh_jscale=0.8, mode_check);

%----------------------------------------------------------------

% generate IRFs for monetary policy shock

%----------------------------------------------------------------

stoch_simul(order = 1,irf=15) y_gap pi_p_ann pi_w_ann w_real y n;

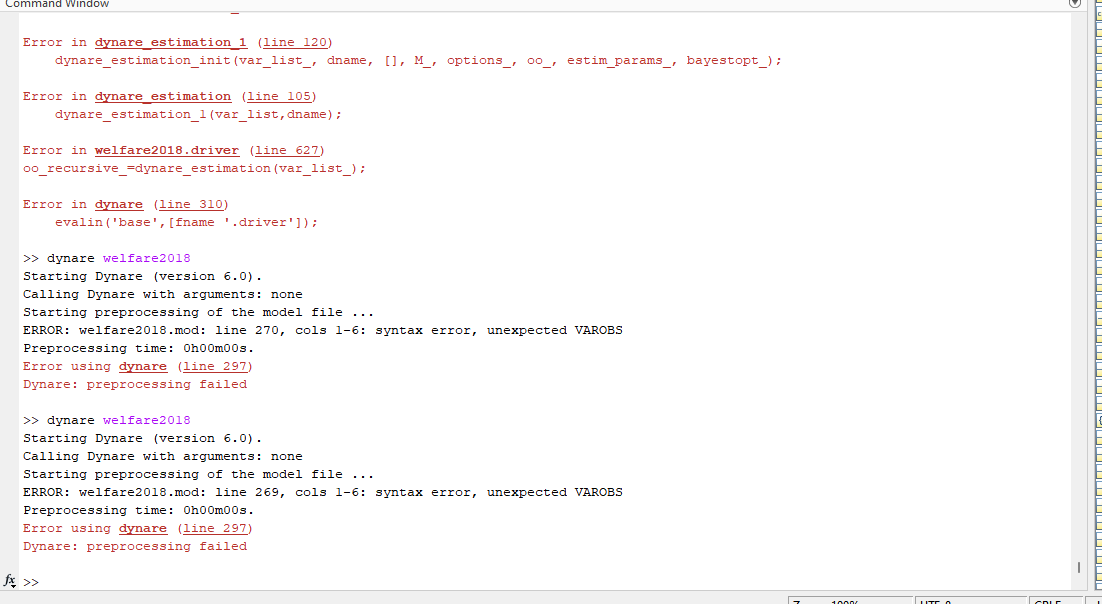

still doesnt work

When you use estimated_params block at the end of this block you should use end;

estimated_params;

betta, normal_pdf, 0.50, 0.01;

rho_z, uniform_pdf, 1, 0.50;

end;

Use this block in your model before the estimation command.

estimated_params_init(use_calibration) ;

end;

And then run the model again.

After the estimation command write endogenous variables names. For example y i c n after the estimation command.

In DSGE models do not use i for investment and use I or Inv or inv .

Do not use MATLAB built-in functions names or similar MATLAB command names because MATLAB may cause problem when you solve the model.

i do not get you.could you please check my mod.i am sharing here again.

welfare2018.mod (11.2 KB)

welfare.xlsx (12.8 KB)

After the estimation command write endogenous variables names for example:

estimation( …) y i c n ;

As the message states, you use

estimated_params_init(use_calibration) ;

end;

to start at beta=0.99. But you set

estimated_params;

betta, normal_pdf, 0.50, 0.01;

With a having a 49 standard deviation difference to the mean of the specified distribution is virtually impossible.

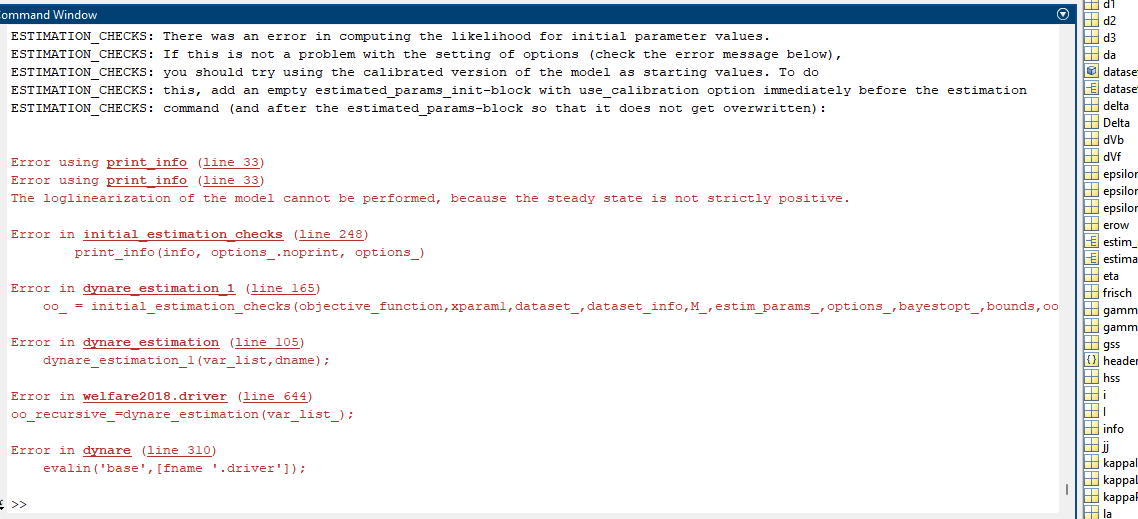

I still don’t know what you are trying to do. But you cannot use the loglinear option in your model due to negative/zero steady states.

Alright Professor.