I have built a 2-country DSGE model in which the household accumulates capital and provides capital and labor effort to his local intermediate firms. The household has the possibility to buy domestic and foreign bonds. To close the economy, foreign bond holdings come along with some costs.

Is my guess correct, that such a model shows complete bond markets but incomplete asset as well as incomplete labor markets because the household is allowed to provide capital and labor effort only in his home country?

When I simulate the model (1% home productivity shock, same home and foreign parameterization), the exchange rate under no bias in trade (trade-openness = 0.5) is constant. Nonetheless, the ratio between home’s marginal utility of consumption to foreign’s marginal utility of consumption ist not unity. I consider the latter fact as the effect of incomplete markets. Is this correct?

I would like to inquire again because I’m confused. You mention that adjustment costs of foreign bond holdings prevent perfect risk-sharing. But then my guess of complete bond markets would be wrong?

I use a model in which domestic and foreign final firms aggregate home and foreign intermediate goods. These goods are imperfect substitutes in the standard case.

After a 2nd order approximation of the nonlinear and no bias in trade, as well as when the subsitutability of home and foreign goods approaches unity, I observe after a home productivity shock, that international output-, consumption-, labor supply-, and investment correlations are equal to 1 (only under this parameterization). I am aware that my simulation is not directly comparable to the theoretical question of complete vs. incomplete markets.

Now, I would say that neither the bond nor the asset markets are complete in my setting. Is this correct? Nonetheless, my simulation under no bias in trade and specific substitutability of home and foreign intermediate goods looks indistinguishable from a complete market setting?

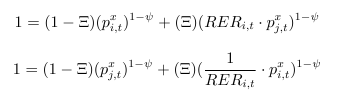

Under the mentioned parameters above (Xi = 0.5, psi = 1), RERi,t = 1 (PPP applies), the equations collapse with the intermediate goods market equilibrium

to

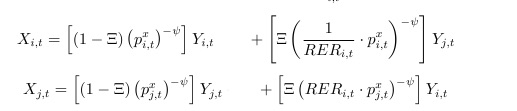

where pi,t^{x} are relative home prices. Xi,t (Xj,t) is the total demand for home’s (foreign’s) intermediate good. In this case, the total real demand for home’s intermediate goods coincides with the total real demand for foreign’s intermediate good.