Hi to all

I am replicating a paper Putting home economics into macroeconomics. Here I am attaching my mod file.

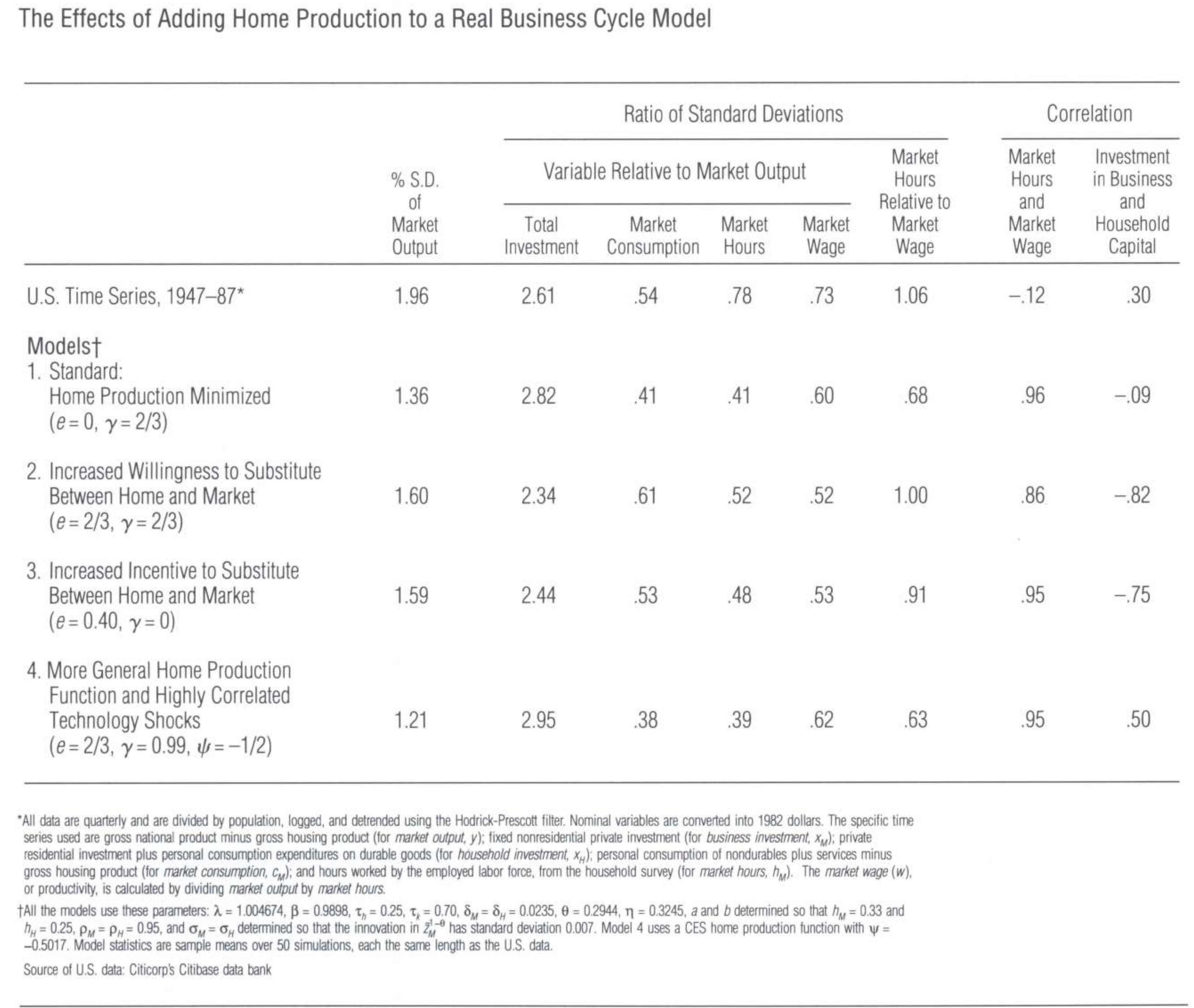

When I compare standard deviations for different endogeneous variables obtained from dynare simulation with the standard deviations reported in the paper. There is very drastic difference.

I read here on the forum and some literature from university courses that Dynare takes the variables as logs.

Can anybody help me in transformation of dynare generated standard deviation into what reported.

e04.mod (3.1 KB)

The reported standard deviations are for the log-levels, not the levels. But you are not considering the logs. See Question about understanding irfs in dynare

Also, it is not clear whether the model moments are also based on HP-filtered model data or whether they are comparing the filtered empirical data to the unfiltered model data.

All the data are quarterly and divided by population, logged and detrended using HP filter nominal variables are converted in to 1982 dollars it is mentioned at the bottom of table present in the paper_

I read that note. But it’s not clear whether that applies to the model data as well. Obviously, in the model there is no population growth, you you cannot divide by population.That then begs whether HP filtering was done. But you should be able to find that out by trying the two possibilities.