it should be pretty easy to replicate, but I keep getting a collinearity issue.

I know that often prices are not determined in these models, but a version of this code with inflation instead of the price level does not solve the problem.

I’m wondering if there is something obvious that I do not immediatly see.

I would greatly appreciate if anoyone could give me his opinion on this. Thanks in advance,

This more seems like an issue with closing the model as a lot of real variables are involved. Either there are still bugs in your coding or there is a conceptual problem (missing equation)

Dear Johannes, yes indeed.

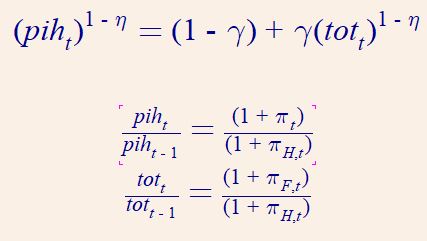

In the end we found a solution over the weekend and now we have a working code. The point was (as often is) to get a correct definition of inflation and prices. The model needs to have on unit root (the nominal exchange rate). To correctly code that in it was necessary to transform intermediate prices in relative prices. Doing that the model works and correctly replicates the IRFs of the paper.

Could you please explain in a bit more details how you fixed this issue or even post your new mod file?

I am facing a similar issue of collinearity due to the definition of prices in another two-country model.

Dear Francois (apologies for the spelling)

My problem was with the definition of prices. Do you have prices defined as relative (i.e. defined the domestically produced fgood price in country 1 as p_d1=[price domestic good]/[price index country 1]).

Let me know if this works,

The trick is almost always to express the model only in terms of inflation rates and relative prices. That is why @Massimo indicated. You define an new variable that stores the relative price and only that price shows up in the model. The reason is that the price of the numeraire is not determined in the model.

Your second question is different. Inflation rates are usually also not endogenously determined in steady state as the Fisher equation implies that many combinations of nominal interest rates and inflation rates are consistent with a given required real interest rate. For that reason, there is a degree of freedom in the model to select a particular steady state inflation rate. With open economy models, it is a bit more complicated as you usually want a stationary exchange rate, which requires real interest rates and inflation rates to be consistent. If the countries are symmetric, assuming a zero inflation steady state is typically a consistent solution.