@TerribleStudent In case of equation (42) above the data is mean 0 by construction. Why is it not in your case?

@Shells What is the error message your are getting in in Matlab 2021?

Sorry, you’re correct, both rates have mean zero (8.081644e-20 to be precise).

I’ve solved most mode_check plots by adjusting the data for inflation (as specified in the manual) and respecified the mean and SD for some priors. It seems the model doesn’t solve/work for some specific values of the parameters (even in stoch_simul) … is this common?

That depends on the reason. It is very common for some parameter vectors to not satisfy the Blanchard-Kahn conditions. But the red dots can be caused by other pathological issues. Setting

options_.debug=1;

should provide more information.

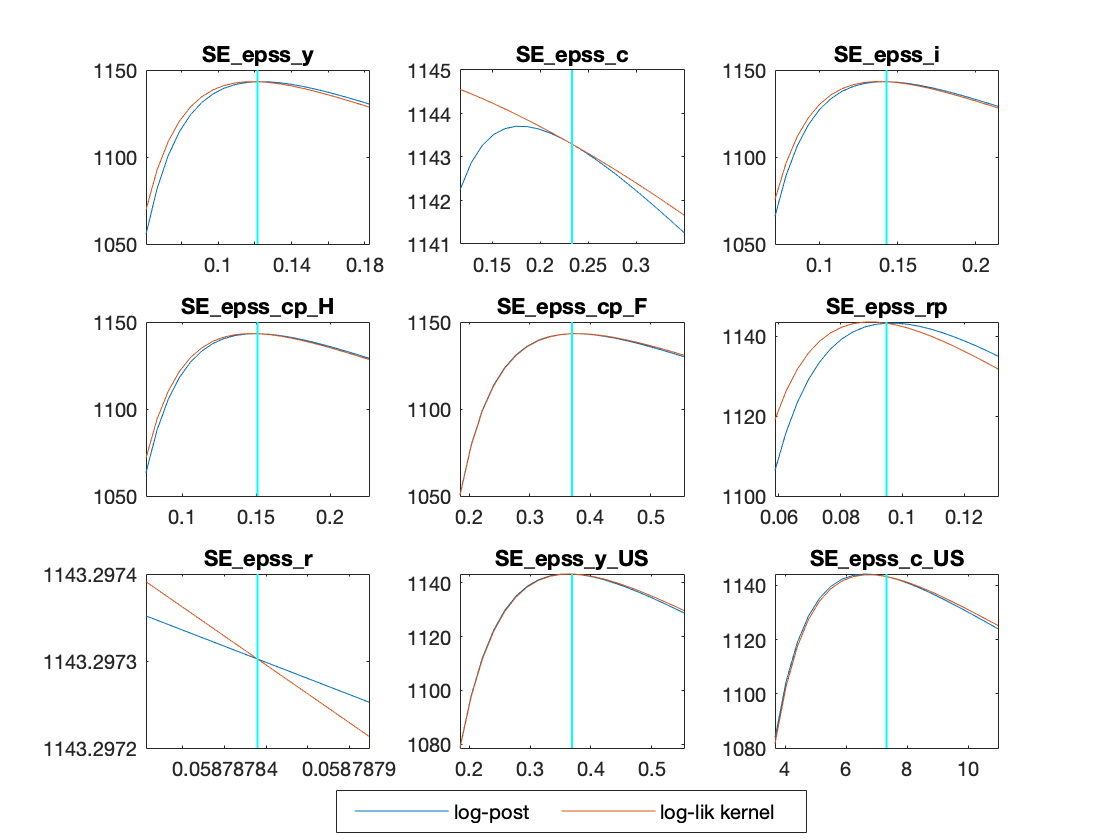

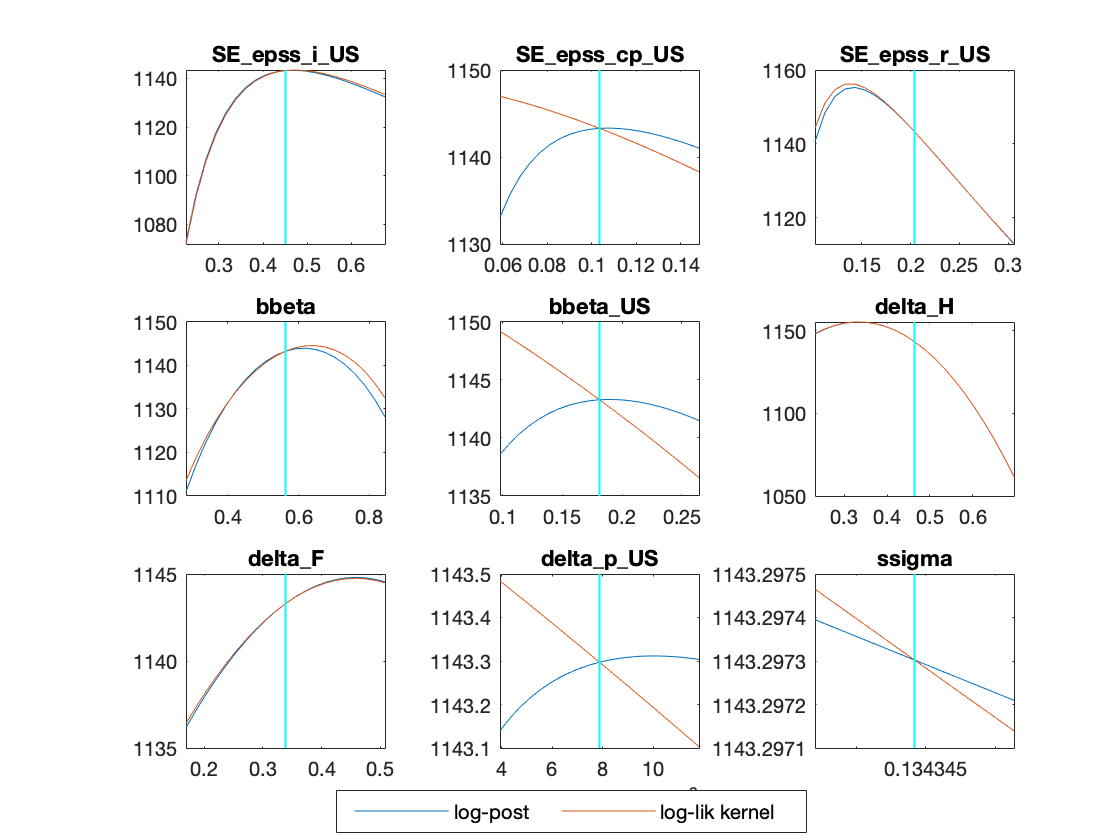

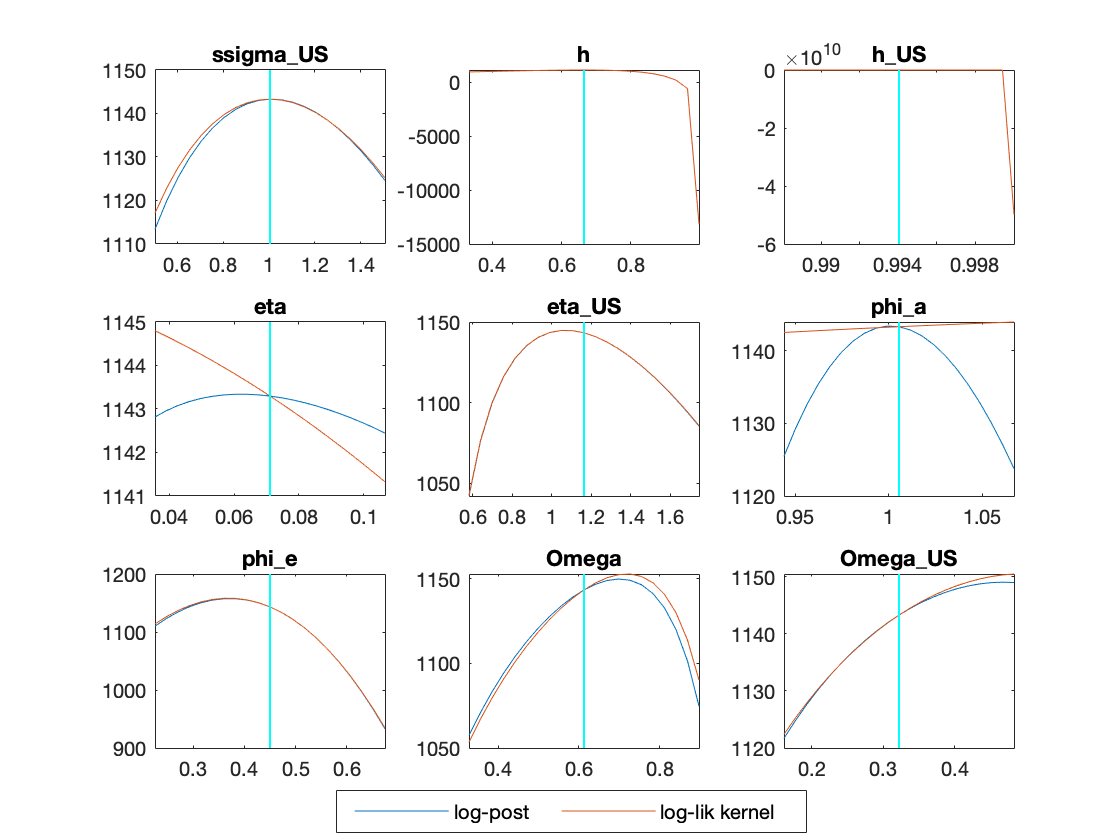

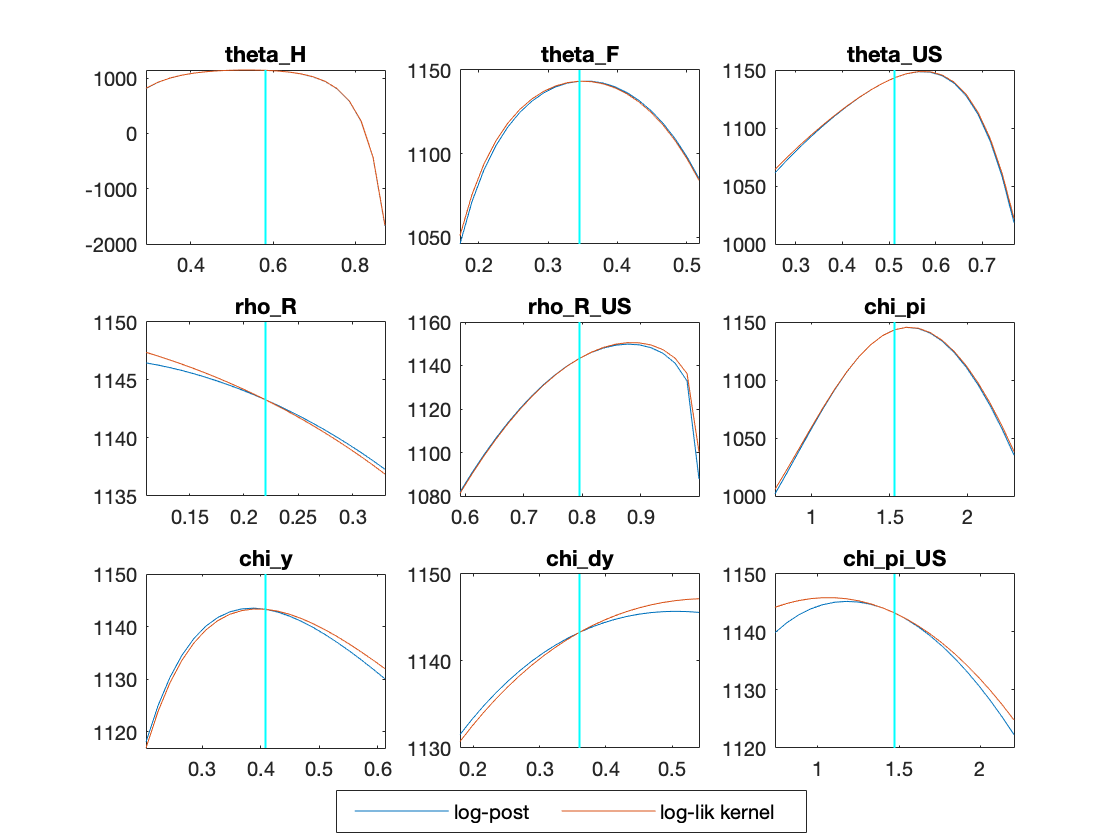

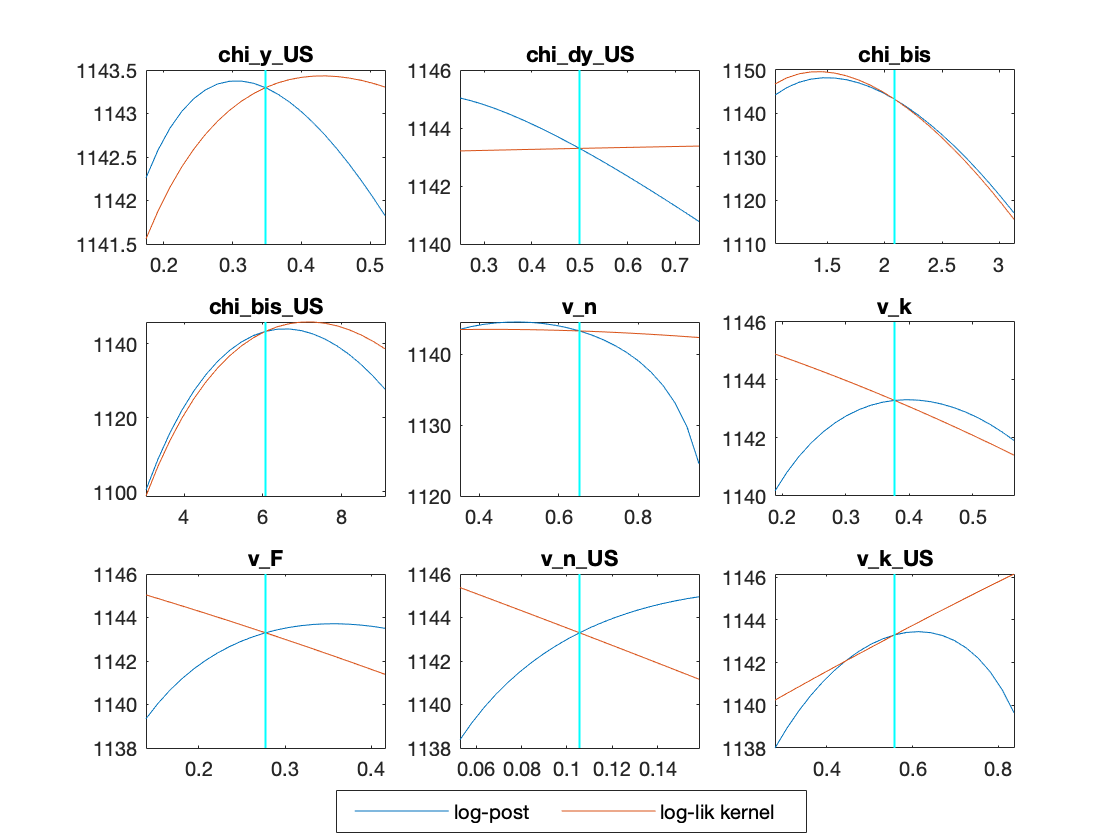

I get these plots currently

and the following messages:

"Estimation::marginal density: Let me try again.

Estimation::marginal density: There’s probably a problem with the modified harmonic mean estimator.

ESTIMATION RESULTS

Log data density is -Inf."

and lastly:

“DsgeSmoother: Switching to univariate filter. This is usually due to co-integration in diffuse filter,

otherwise it may be a sign of stochastic singularity.”

How to interpret it?

">> options_.debug=1

options_ =

struct with fields:

datafile: 'dataset1'

dirname: 'model'

dataset: [1×1 struct]

verbosity: 1

terminal_condition: 0

rplottype: 0

smpl: 0

dynatol: [1×1 struct]

slowc: 1

timing: 0

gstep: [2×1 double]

scalv: 1

debug: 1

initval_file: 0

schur_vec_tol: 1.0000e-11

qz_criterium: []

qz_zero_threshold: 1.0000e-06

lyapunov_complex_threshold: 1.0000e-15

solve_tolf: 6.0555e-06

solve_tolx: 3.6669e-11

dr_display_tol: 1.0000e-06

minimal_workspace: 0

dp: [1×1 struct]

steady: [1×1 struct]

simul: [1×1 struct]

mode_check: [1×1 struct]

huge_number: 10000000

threads: [1×1 struct]

jacobian_flag: 1

steadystate_flag: 2

steadystate_partial: []

steadystate: [1×1 struct]

ParamSubSet: 'None'

dsge_var: 0

dsge_varlag: 4

bvar_replic: 2000

bvar_prior_tau: 3

bvar_prior_decay: 0.5000

bvar_prior_lambda: 5

bvar_prior_mu: 2

bvar_prior_omega: 1

bvar_prior_flat: 0

bvar_prior_train: 0

bvar: [1×1 struct]

optim_opt: []

gmhmaxlik: [1×1 struct]

nointeractive: 0

graphics: [1×1 struct]

graph_format: 'eps'

nodisplay: 0

nograph: 0

no_graph: [1×1 struct]

XTick: []

XTickLabel: []

console_mode: 0

irf: 40

impulse_responses: [1×1 struct]

zero_moments_tolerance: 1.0000e-10

relative_irf: 0

ar: 5

hp_filter: 0

one_sided_hp_filter: 0

filtered_theoretical_moments_grid: 512

nodecomposition: 0

nomoments: 0

nocorr: 0

periods: 0

noprint: 0

SpectralDensity: [1×1 struct]

nofunctions: 0

bandpass: [1×1 struct]

irf_opt: [1×1 struct]

ep: [1×1 struct]

bnlms: [1×1 struct]

particle: [1×1 struct]

rwgmh: [1×1 struct]

TeX: 0

xls_sheet: 1

xls_range: ''

prior_draws: 10000

sampling_draws: 500

forecast: 0

forecasts: [1×1 struct]

conditional_forecast: [1×1 struct]

linear: 1

stack_solve_algo: 0

markowitz: 0.5000

minimal_solving_periods: 1

endogenous_terminal_period: 0

no_homotopy: 0

pfwee: [1×1 struct]

order: 1

pruning: 0

solve_algo: 4

replic: 50

simul_replic: 1

drop: 100

aim_solver: 0

k_order_solver: 0

partial_information: 0

ACES_solver: 0

conditional_variance_decomposition: []

ramsey_policy: 0

instruments: {}

timeless: 0

ramsey: [1×1 struct]

initial_period: NaN

no_init_estimation_check_first_obs: 0

Harvey_scale_factor: 10

heteroskedastic_filter: 0

MaxNumberOfBytes: 100000000

MaximumNumberOfMegaBytes: 111

analytic_derivation: 0

analytic_derivation_mode: 0

bayesian_irf: 1

bayesian_th_moments: 0

diffuse_filter: 1

filter_step_ahead: []

filtered_vars: 0

smoothed_state_uncertainty: 0

first_obs: 1

nobs: 106

kalman_algo: 0

fast_kalman_filter: 0

kalman_tol: 1.0000e-10

kalman: [1×1 struct]

diffuse_kalman_tol: 1.0000e-06

use_univariate_filters_if_singularity_is_detected: 1

riccati_tol: 1.0000e-06

lik_algo: 1

lik_init: 3

load_mh_file: 0

load_results_after_load_mh: 0

logdata: 0

loglinear: 0

linear_approximation: 0

logged_steady_state: 0

mh_conf_sig: 0.9000

prior_interval: 0.9000

mh_drop: 0.5000

mh_jscale: 0.1802

mh_tune_jscale: [1×1 struct]

mh_init_scale: 0.4000

mh_initialize_from_previous_mcmc: [1×1 struct]

mh_nblck: 2

mh_recover: 0

mh_replic: 20000

recursive_estimation_restart: 0

MCMC_jumping_covariance: 'hessian'

use_calibration_initialization: 0

endo_vars_for_moment_computations_in_estimation: []

occbin: [1×1 struct]

silent_optimizer: 0

prior_restrictions: [1×1 struct]

mode_compute: 6

mode_file: ''

moments_varendo: 0

nk: []

noconstant: 0

nodiagnostic: 0

mh_posterior_mode_estimation: 0

prefilter: 0

presample: 0

prior_trunc: 1.0000e-10

smoother: 0

smoother_redux: 0

posterior_max_subsample_draws: 1200

sub_draws: 1200

ME_plot_tol: 1.0000e-06

use_mh_covariance_matrix: 0

gradient_method: 2

gradient_epsilon: 1.0000e-06

posterior_sampler_options: [1×1 struct]

trace_plot_ma: 200

mh_autocorrelation_function_size: 30

plot_priors: 1

cova_compute: 1

parallel: 0

parallel_info: [1×1 struct]

number_of_grid_points_for_kde: 512

conditional_variance_decomposition_dates: [1 5 9 13 17 37 77 117 157 197]

filter_covariance: 0

filter_decomposition: 0

selected_variables_only: 0

contemporaneous_correlation: 0

initialize_estimated_parameters_with_the_prior_mode: 0

estimation: [1×1 struct]

homotopy_mode: 0

homotopy_steps: 1

homotopy_force_continue: 0

rescale_prediction_error_covariance: 0

hessian: [1×1 struct]

csminwel: [1×1 struct]

newrat: [1×1 struct]

simplex: [1×1 struct]

cmaes: [1×1 struct]

simpsa: [1×1 struct]

solveopt: [1×1 struct]

saopt: [1×1 struct]

particleswarm: [1×1 struct]

prior_mc: 20000

prior_analysis_endo_var_list: {}

block: 0

use_dll: 0

bytecode: 0

sylvester_fp: 0

sylvester_fixed_point_tol: 1.0000e-12

lyapunov_fp: 0

lyapunov_db: 0

lyapunov_srs: 0

lyapunov_fixed_point_tol: 1.0000e-10

lyapunov_doubling_tol: 1.0000e-16

dr_cycle_reduction: 0

dr_cycle_reduction_tol: 1.0000e-07

dr_logarithmic_reduction: 0

dr_logarithmic_reduction_tol: 1.0000e-12

dr_logarithmic_reduction_maxiter: 100

initial_date: [1×1 dates]

discretionary_policy: 0

discretionary_tol: 1.0000e-07

parameter_set: []

use_shock_groups: ''

shock_decomp: [1×1 struct]

plot_shock_decomp: [1×1 struct]

nonlinear_filter: []

ms: [1×1 struct]

graph_save_formats: [1×1 struct]

endogenous_prior: 0

endogenous_prior_restrictions: [1×1 struct]

osr: [1×1 struct]

gpu: 0

convergence: [1×1 struct]

marginal_data_density: [1×1 struct]

lmmcp: [1×1 struct]

lcppath: [1×1 struct]

mcppath: [1×1 struct]

figures: [1×1 struct]

varobs_id: [41 42 43 44 45 46 47 48 49 50]

pac: [1×1 struct]

DynareRandomStreams: [1×1 struct]

varobs: {10×1 cell}

varlist: {8×1 cell}

number_of_observed_variables: 10

B: 1200

"

There are 21 eigenvalue(s) larger than 1 in modulus

for 22 forward-looking variable(s)

The rank condition ISN’T verified!

Error using print_info (line 32)

Blanchard & Kahn conditions are not satisfied: indeterminacy.

Error in stoch_simul (line 107)

print_info(info, options_.noprint, options_);

Error in US_IC3_v2.driver (line 1185)

[info, oo_, options_, M_] = stoch_simul(M_, options_, oo_, var_list_);

Error in dynare (line 293)

evalin(‘base’,[fname ‘.driver’]) ;

@Shells So you are saying the model ran without the BK violations in Matlab 2017, but not in 2021? If that is the case, please provide the file.

@TerribleStudent The options_.debug=1; will lead to additional output during mode_check of red dots appear. This is not the case here. It seems rather that you are missing

prior_trunc=0;

It was running fine in matlab 2017 (without the BK errors) yes. After the matlab update, I have tried too many different versions of the mod file however, so I am not sure anymore what the exact original version was. Except of course I am still getting the BK-related errors. The latest mod file of course is attached in my very first comment/question above - just not sure if it is the exact same one that was giving me no errors in matlab 2017. Sorry!

I’m getting more red dots with prior_trunc=0 which I have trouble solving. This is my estimation settings

estimation(datafile=dataset1, first_obs=1, mh_replic=10000, mh_nblocks=2, mh_drop=0.5, mh_jscale=0.4, mode_compute=6, mode_check, bayesian_irf, diffuse_filter, prior_trunc=0) y c i n pi r tot rer;

any suggestions or ideas? I’m attaching my code/data if anyone have time to check. Thank you.

dataset1.mat (8.7 KB)

model.mod (7.7 KB)

The red dots mostly indicate that your model is very close to the boundary to instability.

Can that be solved by using upper- and lower bounds on the priors?

Not really. You would be replacing one corner solution with another bound, i.e. an implicit prior with an explicit one. Rather, you would need to make the prior more informative, or even better try to understand why the data prefers something close to instability.

Thank you for all your help, the only issue currently is that some of the Brooks and Gelman (1998) plots doesn’t converge, I guess thats also related to the priors, I’ll keep investigating.

I do have one question not related to the part above: Is it okey to report in a paper/thesis the “Variance decomposition (in percent)” obtained from the stoch_simul and bayesian irf from the estimation command? Or shouldn’t one mix them?

I’m interest in the estimation of the parameters, bayesian irf and variance decomposition, but what I’ve read on the forum it’s hard to interpret the VD from the estimation command.

I’ll then use the following commands

estimation(datafile=dataset1, first_obs=1, mh_replic=20000, mh_nblocks=2, mh_drop=0.5, mh_jscale=0.3, mode_compute=6, mode_check, bayesian_irf, diffuse_filter, prior_trunc=0) y c i n pi r tot rer;

stoch_simul(order=1, irf=0) y i pi r tot rer y_US i_US pi_US r_US;

Edit; One of my variables doesn’t show up in the VD in stoch_simul, namely i_US what could be the reason?

Sincerely,

TerribleStudent

- Both objects (the mean variance decomposition over the posterior parameters from

estimationand the variance decomposition for the mean parameter draw fromstoch_simul) measure different things. Thus, you should not mix them but rather use the one that is most suitable for your application. - DId you check whether the variance of

i_USis neither 0 nor infinity?

-

So I shouldn’t mix the bayesian irf with the variance decomposition obtained from the stoch_simul, rather choose between bayesian irf and mean variance decomposition or irf and VD from stoch_simul with the estimated parameters?

-

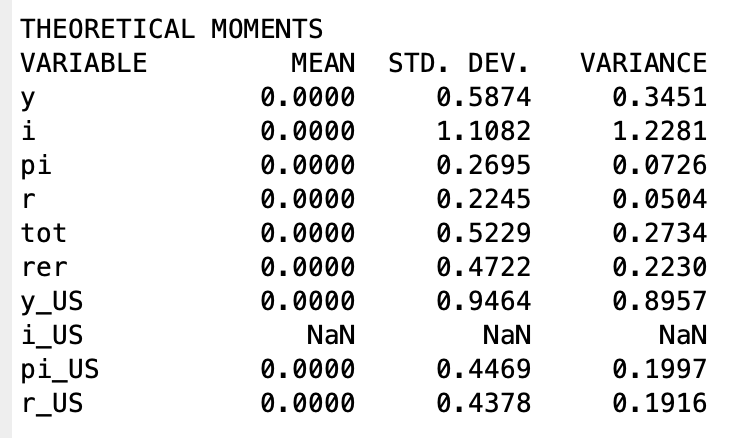

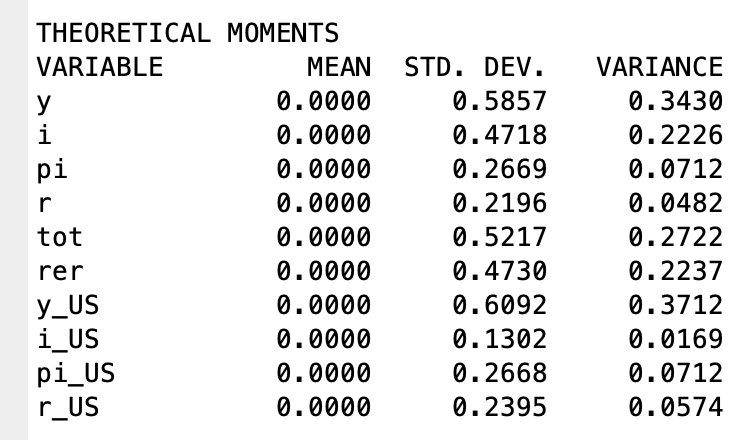

There is some problem with mean, SD and variance, what could possible be the reason for this?

EIGENVALUES:

Modulus Real Imaginary

4.344e-17 -4.344e-17 0

9.928e-17 -9.928e-17 0

0.2701 0.2701 0

0.2799 0.2799 0

0.4071 0.3452 0.2158

0.4071 0.3452 -0.2158

0.5398 0.3356 0.4228

0.5398 0.3356 -0.4228

0.5541 0.4626 0.305

0.5541 0.4626 -0.305

0.595 0.4721 0.3622

0.595 0.4721 -0.3622

0.7503 0.7503 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8 0.8 0

0.8359 0.8336 0.06173

0.8359 0.8336 -0.06173

0.976 0.976 0

0.9966 0.9966 0

1 1 0

1.045 1.045 0

1.192 1.163 0.2594

1.192 1.163 -0.2594

1.194 1.194 0

1.382 1.382 0

1.603 1.603 0

2.029 2.029 0

2.041 2.041 0

2.817 2.461 1.371

2.817 2.461 -1.371

3.677e+16 -3.677e+16 0

1.065e+17 1.065e+17 0

1.172e+17 1.172e+17 0

1.998e+17 -1.998e+17 0

3.027e+18 -3.027e+18 0

There are 15 eigenvalue(s) larger than 1 in modulus

for 15 forward-looking variable(s)

The rank condition is verified.

- Sorry, I meant you wanted to combine the same object (variance decomposition) from

stoch_simulandestimation. What you suggest should be fine as long as you clearly outline it. But note that a referee may prefer you to be fully Bayesian. - I outlined the two reasons:

i_USmay be constant so that the variance is 0 or it may have a unit root so that the variance is infinite.

-

Yes, thats what I thought.

-

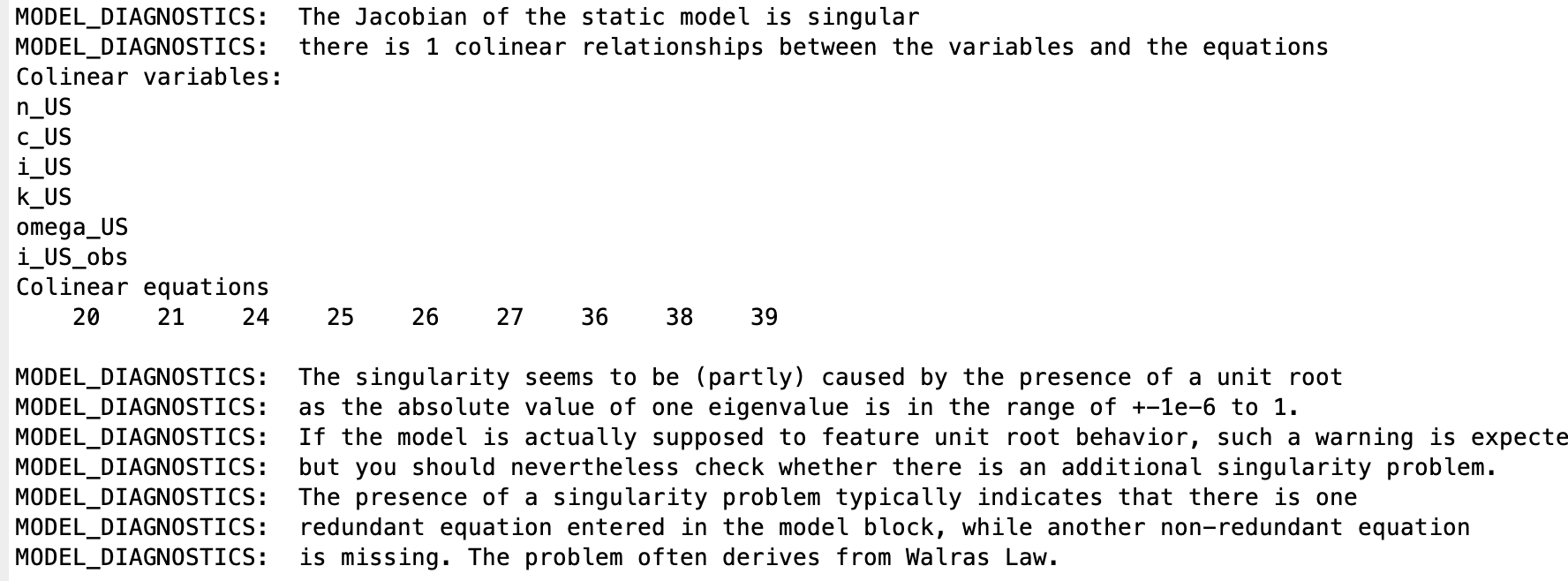

So when I run the model_diagnostics(M_,options_,oo_) I get the following

the i_US equation is specified as

i_US=(1/(1+bbeta_US))*i_US(-1)+(bbeta_US/(1+bbeta_US))*i_US(+1)+(1/(chi_bis_US*(1+bbeta_US)))*(q_US+eps_i_US);

which is the same as for the domestic i variable equation. However, when I remove either (1/(1+bbeta_US))*i_US(-1) or (bbeta_US/(1+bbeta_US))*i_US(+1) I get the following in the model_diagnostics

![]()

and i_US shows up in both the theoretical moments and VD etc.

So my question are:

-

why would excluding the

(1/(1+bbeta_US))*i_US(-1)part from the foreign investment equation solve the problem when it works for the domestic? Also this is a common investment equation in the literature where both i(-1) and i(+1) is present, for example Smets and Wouters. -

also this means I change some key equations which means its not consistent with the log-linearization process by pen and pencil, how should one proceed?

-

this indicate that (at least) 2 equations in this published paper is falsely.

Please provide the mod-file.

- The two terms make sure that they sum to 1. I am not familiar with the model, but a unit coefficient can cause something like this if the rest of the model does not induce stationarity.

- The big question is if the unit root is really a problem, i.e. if it’s a bug or a feature.

- Again, that depends on whether the published equation is really wrong or whether it is correct, but induces a unit root.

True. And the model works, but I do get a message after the estimation of a possible issue.

I could exclude the foreign variables in the VD since I’m mostly interested in the domestic ones etc

dataset1.mat (8.7 KB)

model.mod (7.9 KB)

.

It’s hard to tell what is going on in this model, but dropping the foreign sector may be a solution.