Hello everybody!

I would like to compute the Baxter and King filter of output in the model section treating it as an endogenous variable, say Y_BK. Is it possible to do something like this in dynare?

Hello everybody!

I would like to compute the Baxter and King filter of output in the model section treating it as an endogenous variable, say Y_BK. Is it possible to do something like this in dynare?

From what I can see, the Baxter/King filter has a state space representation that you could use to manually define the filtered output in your model.

Where can I find the formula for its state-space representation?

Their paper shows how to compute the moving average weights.

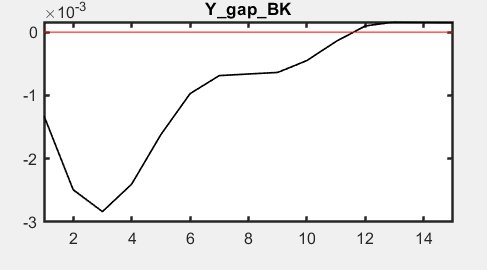

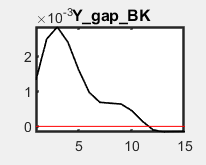

So, I computed them and them used stoch_simul; but the IRFs I get look strange:

Attached you can find my .mod file.

NK_Model.mod (6.9 KB)

Comparing your computed weights to the one used in Matlab’s bkfilter.m, you flipped the order of lower and upper cutoff. It should be:

p_l = 32;

p_h = 6;

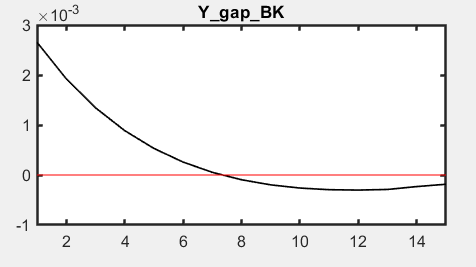

My hunch is that the approximation to the passband may become smoother as well.

Thank you very much Professor! You have been really helpful ![]()