Dear All

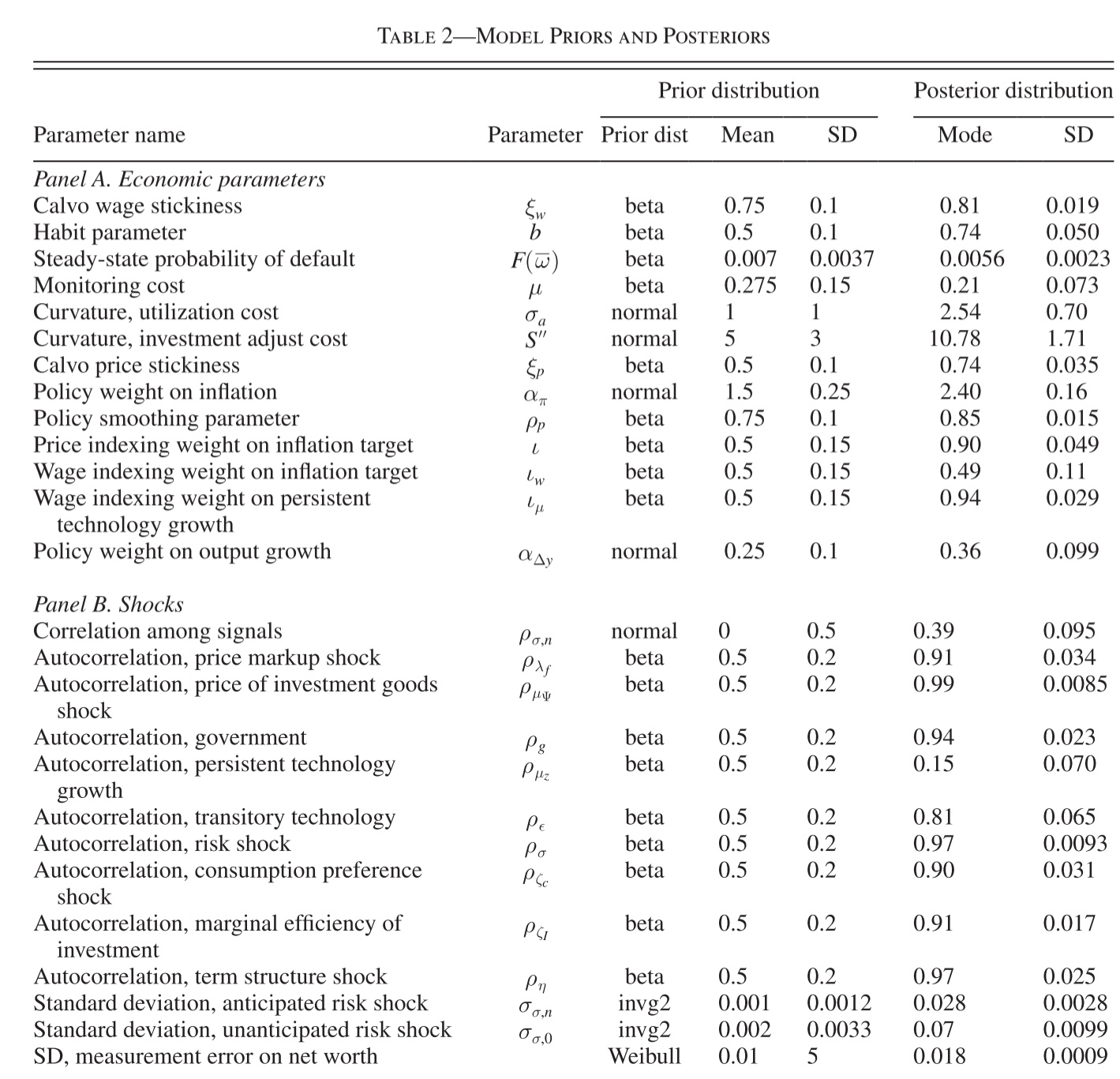

I estimated the model with five shocks, but some shocks are not quite persistent. Is this a sign of problem especially the “rho_a” ?

Thank u very much

Swift

I do not understand your problem here. What is a “sign problem”? All the posterior means are found positive. A negative autoregressive parameter may be a problem, because it would imply oscillatory Impulse Response Functions, but it is not what you show here.

The fact that the exogenous variables are less persistent than usual is not necessarily an issue. I do not know your model nor the data, but low autocorrelation in the exogenous variables, means that you have enough endogenous persistence in the model to match the persistence in the data. So your result can be explained by low persistence in the data or by the endogenous persistence in the model (which is a good point for your model). Obviously it is hard to conclude anything since we do not know how you estimated the model (for instance, did you check the convergence of the MCMC?).

Without information on the economic interpretation of shocks, it is hard to tell. Are your posterior estimates much lower than in comparable papers in the literature?

As I can see from Risk Shocks(CMR2014) etc, my results are lower. I don’t think its a problem now bc the model and data is different.

Thank u.

Posterior Estimates of Risk Shocks