Areosa W D , Areosa M B M . The inequality channel of monetary transmission[J]. Journal of Macroeconomics, 2016, 48.

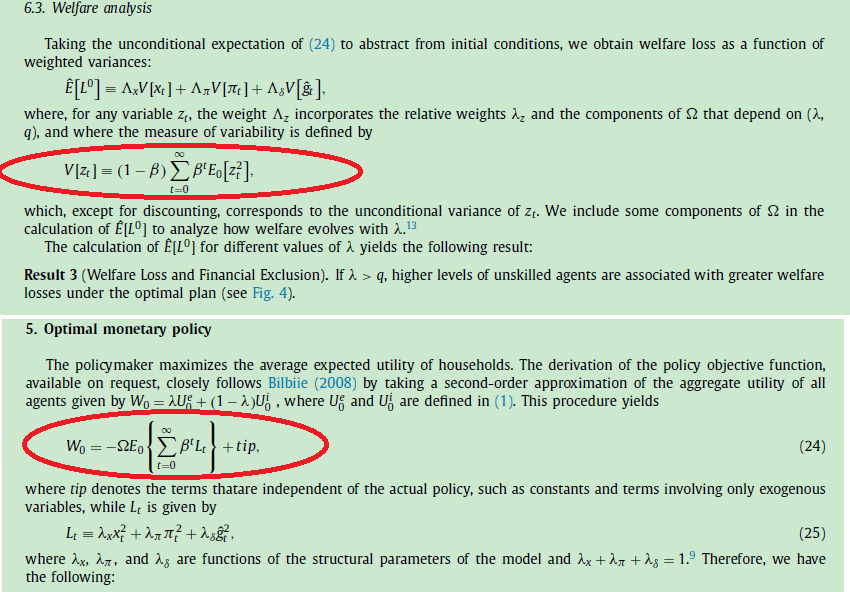

Anybody has the idea how the authors calculate welfare loss in section 6.3 using Dynare? The welfare loss is defined as a infinite series of unconditional variance of the output gap, inflation and inequality. My question is we only get one unconditional variance for each variable endogenous variable. But how can we get infinite many?

Thank you for help!

The inequality channel of monetary transmission_2016_JM.pdf (987.6 KB)

best

You are misreading something. E_0 is not the unconditional variance. My guess is that the defined

V(z_t) recursively, using

\begin{align}

V(z_t)=(1-\beta)\sum_{t=0}^\infty \beta^tE_0[z_t^2]&=(1-\beta)z_0^2+(1-\beta)\sum_{t=1}^\infty \beta^tE_0[z_t^2]\\

&=(1-\beta)z_0^2+\beta(1-\beta)\sum_{t=0}^\infty \beta^{t}E_0[z_{t+1}^2]\\

&=(1-\beta)z_0^2+\beta E_0 V(z_{t+1})

\end{align}

Thank you! @jpfeifer! I know it can be defined recursively. The question is that I do not know which one stand for unconditional variance of z_t.

The author said that V(z_t) , which, except for discounting, corresponds to the unconditional variance of z_t. So it is my understanding that V(z_t) is unconditional variance if E_0[z_t] is not unconditional variance of z_t. Am I right?

E_0 is a conditional, not an unconditional expectation. If that expectation were unconditional then the expression above would simply reduce to

V(z_t)=E(z_t^2)

which is indeed the definition of the unconditional variance.