Hello! I have built a log-linearized NK model and want to analyze forward guidance policy by introducing a shock, for example, in period 5. However, when I use the following command:

var e_cb;

periods 5;

values 0.01;

Dynare gives the following error:

“All endogenous are constant or non-stationary, not displaying correlations and auto-correlations.”

At the same time, if I use the standard command:

var e_cb; stderr 1;

everything works correctly.

Could you please help me fix this issue?

You are confusing perfect_foresight and stochastic simulations. Forward guidance is usually implemented in the former context, where stoch_simul is not applicable.

I modified the model to use the perfect foresight algorithm:

var e_cb;

periods 8;

values 0.01;

end;

steady;

check;

perfect_foresight_setup(periods=300);

perfect_foresight_solver;

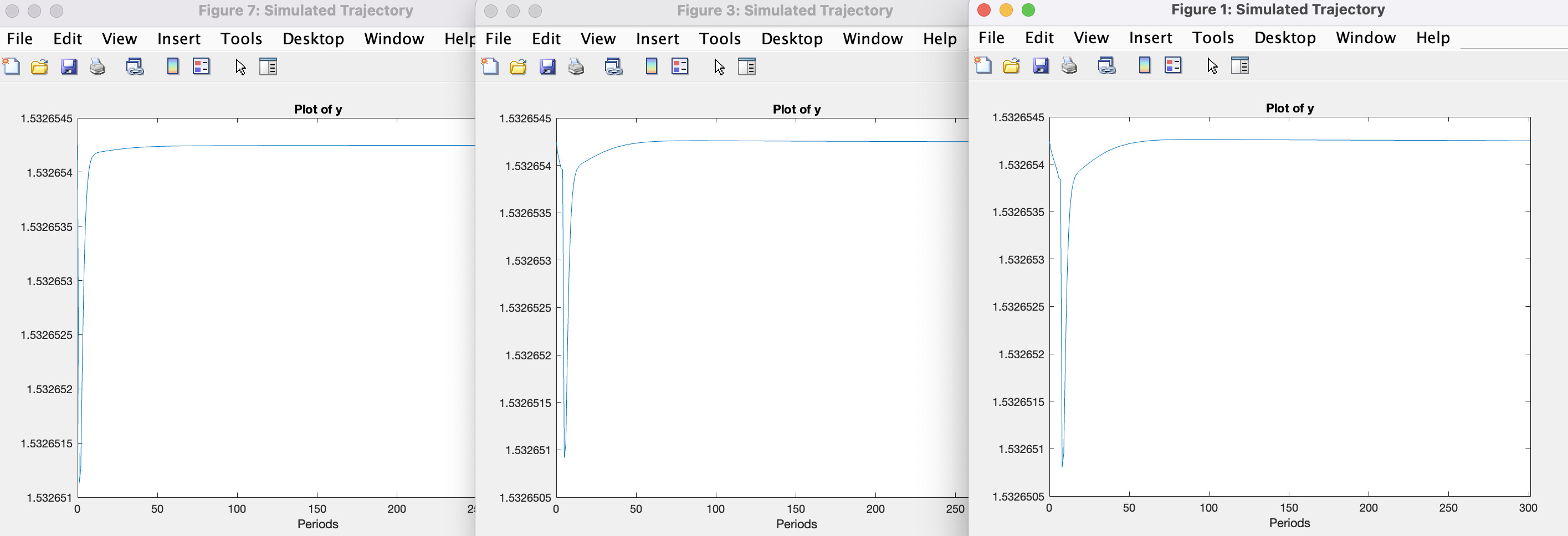

rplot y;

rplot pi;

The response of output in periods 1, 5, and 8 looks as shown in the graph. In every case, the trajectory starts from the same point in period zero. According to the forward guidance paradox, the further in the future an interest rate change is planned, the stronger the variables react today. Could you clarify whether my model addresses this paradox (I’m incorporating various nominal and real rigidities to handle it), or if my model is not functioning correctly? I haven’t included the ZLB, as the main goal of the work does not focus on that.

I don’t know a lot about the model, but the movement in y is tiny.

Anyway, thank you for your help!