Hi everyone, I have a question.

I find that when we test a positive financial shock in a open economy model (which means the domestic entreprenuer wealth suddenly increases), the IRFs show that the cross-border capital always flows in with the exchange rate depreciating and domestic interest rate going up! It looks unrealistic, as we know when the domestic interest rate goes up, the exchange rate will appreciate. Many papers show this odd results, like CTW (2011)

I have test other financial shocks in open economy model, like risk shock in CMR (2014), the capital quality shock in GK (2011), all the results are counterintuitive. It seems the open economy models are only suitable for analysing world interest rate shock or risk premium shock, as these two shocks always create understandable IRFs, that is, the capital always outflow with the depreciating exchange rate and rising interest rate.

Professor jpfeifer, sorry, I may not be making myself clear.

What I mean is that, when there is a rise of the probability of enterprise bankruptcy (which is a positive risk shock in CMR 2014), it should lead to the decreasing output and interest rate, then the capital will outflow and the exchange rate will depreciate. These results are proven in reality or empirical research. Other related financial shocks like negative entreprenear wealth shock in CTW 2011 or negative capital quality shock in GK 2011 should also give the same results, but I found most open DSGE model seems unable to show this feature. In their model, a rise of the probability of enterprise bankruptcy will lead to the decreasing output and interest rate, then the capital will outflow and the exchange rate will apreciate!. I want to know why. looking forward for your reply!

The exchange rate (as well as your intuiton) are governed by the Uncovered Interest Rate Parity condition (UIP). CTW have modified this condition in an ad-hoc way (as they state in the paper) in order to match some empirical pattern in the data. I guess that this modification is what invalides the standard UIP results (interest rates up = appreciation of the domestic currency).

Thanks for your reply . But actually, when we build a similar open economy, we can find that the CTW’s modification isn’t what invalides the standard UIP results. Without their ad-hoc assupmtion, we still can not get the standard results (interest rates up = appreciation of the domestic currency). So in my opinion, they did this assumption and listed the empirical pattern in the data just for trying to defend their strange IRFs. I believe there must be some other reasons behind .

If you read the paper they give the exact reason why they do this. They argue that UIP does not hold perfectly and try to match empirical IRFs for monetary policy shocks.

Yes, I have read their paper. I have build a open model without their ad-hoc assupmtion and found similar results with theirs. So this is why I don’t believe they firstly consider that UIP does not hold perfectly then try to make the ad-hoc assupmtion to match empirical data. I believe they firstly get the odd results then think of a reason to explain the IRFs.

I cant quite follow. You did build a model, where UIP holds perfectly and then a financial shock induces a fall in the interest rate alongside an appreciation of the currency? To me that seems like a violation of the UIP equation.

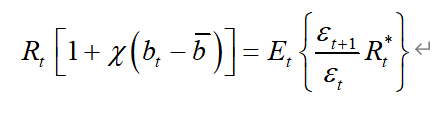

Yes! this is what I meant! I know it seems like a violation of UIP condition, but it isn’t. because there is a adjustment cost about foreign bond bt in the UIP:

So, when the interest rate falls with an appreciation of the currency, the foreign bond investment bt increases, making the UIP equation holds.

In this process, the foreign interest rate holds still.

Now I am lost. If you have a shock that affects bonds b_t it will drive a wedge between the usual UIP condition. Why is that a problem? Empirically, we know that even the covered interest parity condition fails.

Dear professor, I don’t mean this is a problem. What I mean is that, when a shock makes domestic interest rate Rt falls, I find the foreign bond purchased bt increases, which makes sense. But, I also find that the exchange rate εt decreases, meaning currency appreciation (the UIP condition sitll holds as εt+1 decrease more and εt+1/εt decrease). I think this doesn’t match reality because domestic interest rate should decrease with capital outflow and exchange rate depreciation. This is what I think the problem is.

I don’t know if I make myself clear .

With a capital outflow, net indebtedness of the economy increases and therefore the risk premium increases. This increases the risky interest rate relevant for investors, despite the risk-free interest rate R_t going down. If the domestic risky interest rate goes up, the exchange rate can appreciate today as you require an expected depreciation to compensate for the higher domestic interest rate.

I see . Thanks prefessor, you give me a good and possible explaination of my model results. Although I am not sure if this can be modeled by my model, but I will try it!

I cant quite follow. You did build a model, where UIP holds perfectly and then a financial shock induces a fall in the interest rate alongside an appreciation of the currency? To me that seems like a violation of the UIP equation..