Hi, All

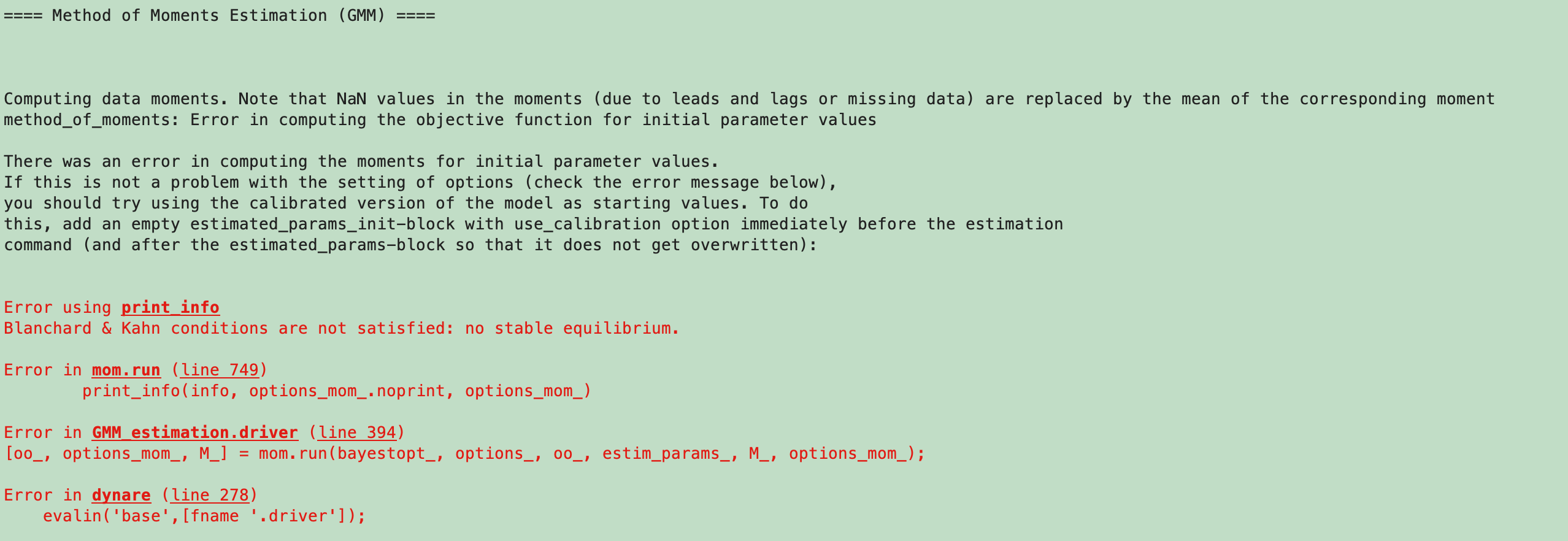

I have a question regarding the GMM estimation. When I run the mod file, I get a message as follows.

I don’t understand how the violation of the BK condition occurs. My model is an NK model of a small open economy with tradable and non-tradable goods. Two nominal variables are not stationary in my model: the non-tradable good price and the nominal exchange rate. Besides these, all the other variables are stationary. I ENCOUNTERED THIS ISSUE when I was trying to match the moments regarding stationary variables. Can you help me figure out how it can occur? I have tried to run the model using the calibrated parameters (excluding the estimation and moments-matching parts and just run the model under the basic parameter configuration, which works without violating the BK condition). Therefore, I feel confused and need some clarification.

Attached are the .mod file and the data.

database.xlsx (16.3 KB)

GMM_estimation.mod (3.3 KB)

Thank you!