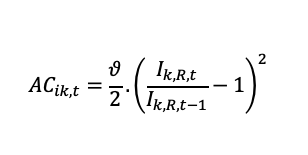

I have a model with quadratic investment adjustment costs:

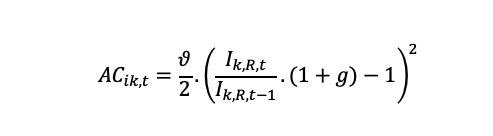

If I detrend the model by growth (1+g), I get the following detrended adjustment cost function:

But this function does not give me ac_ik=0 along the BGP. Hence, in order to have ac_ik=0 at SS, should I specify in the trend model that the adjustment cost function is the following:

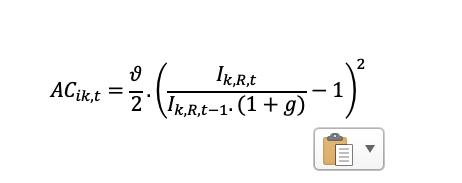

There are two alternative, equivalent ways: AC_{ik,t}=\frac{\vartheta}{2}\left(\frac{I_{k,R,t}}{I_{k,R,t-1}(1+g)}-1\right)^2

or AC_{ik,t}=\frac{\theta}{2}\left(\frac{I_{k,R,t}}{I_{k,R,t-1}}-(1+g)\right)^2=\frac{\theta(1+g)^2}{2}\left(\frac{I_{k,R,t}}{I_{k,R,t-1}(1+g)}-1\right)^2

so that \vartheta=\theta(1+g)^2

Given that 1+g is usually small, it often does not matter. But the typical way is to have the first specification and treat \vartheta as the parameter from the detrended version of the model, i.e. keeping it at 1.5