In my growth model, my real interest rate on bonds at BGP is given by the rental rate of capital minus the depreciation rate of capital. My issue is that it gives an interest rate of 5,3%; way above the observed long term interest rate from the last 25 years.

What to do in that case as the BGP value does not reflect reality?

My low depreciation rate stems from the fact that I have a growth model hence I am subtracting from the steady state capital depreciation rate the growth rate of my economy.

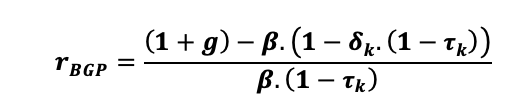

Here are the equations at BGP,

depreciation rate = (investment/capital stock) - growth rate of the economy

This gives a depreciation rate of 0.025

The rental rate of capital is given at BGP by the following equation,

g is the growth rate of my economy, beta the actualisation rate, delta the depreciation rate and tau k the capital tax.

I have an actualisation rate of 0.983, so it is not that low. I calibrated it from the capital Euler equation and the capital demand.

The rental rate of capital is at 7.9%.

I don’t see how I could change the calibration. What would you recommend?

Then your economy is not on the BGP according to our model. Obviously, the depreciation rate, the growth rate, the investment to capital ratio and the tax rate are inconsistent with the observed interest rate.

Okay so that means that actual interest rates are far too low compared what’s a BGP for my model (an interest rate of 5ish%).

Should I write down in the initval block that 5ish% interest rate and then shock that interest rate in the endval block so that it gets a low value? (Im in a deterministic set up).

That may be one way to go. You need to decide along which margin the convergence to the BGP has not happened yet. The problem with initval is that the interest rate is not a state variable, so the initial value cannot be set.

Thank you. I’m going to try to shock the interest rate, or try to re-calibrate the model. But I’m afraid the interest rate (on bonds) that I will find will still not reflect today’s low rates.

If I fix the actualisation rate according the actual long term interest rate I get an actualisation rate above 1…

I’m going to go with option 1: shocks to interest rates on bonds.

I am jumping back on this matter. When calibrating r such that beta equals 0.99, i find a rental rate fo capital (r) of 15.7%. Not that this rental rate takes into account the rate of growth of the economy and taxes on capital income (about 30%). And actually, if I suppose that, from national account data and tthe identity GDP = compensation to employees + operating surplus + compensation of fixed capital; (operating surplus + CFC)/total capital stock of my economy gives me a rental rate of 15.7% too.

I have a simple (deterministic) dsge model, with no finance/banking sector.

But I find this r to be very high, though in my model it does not reflect long run interest rates, but really the rental rate of capital given that households need to replace of share of it each year and pay taxes on capital income.

It is annually. The depreciation rate of the capital of my economy is about 7.7% and the taxation of capital 28.4%, which leads to actually a real rental rate of 12.5% (not 15.7%).

Normally I always find something around 7%, but with a depreciation rate of 2.5%. However, the economy I’m looking at has a very high depreciation rate of K.