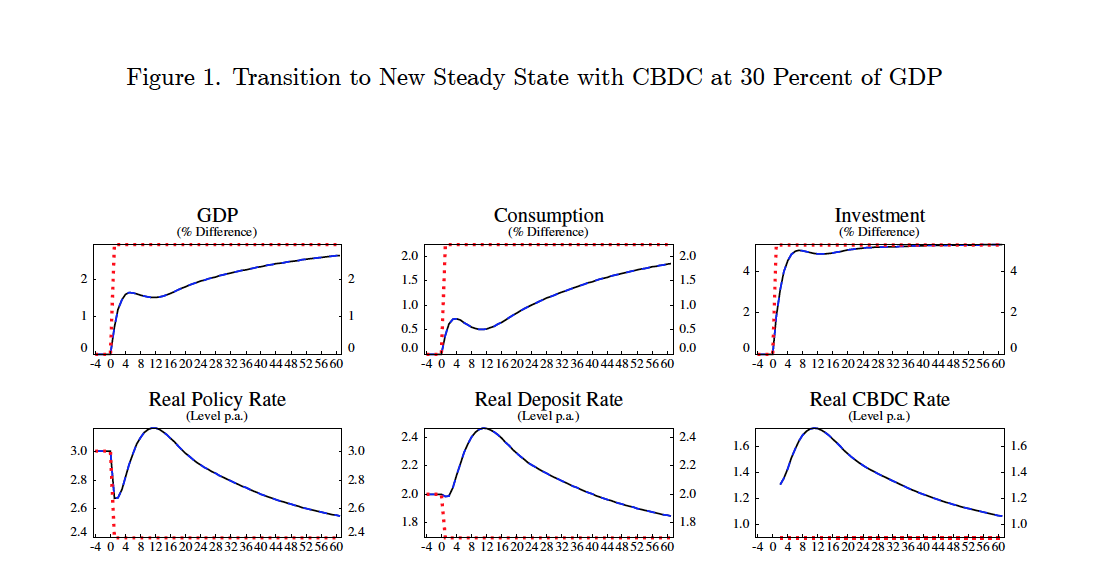

I was trying to replicate the paper by John Barrdear and Michael Kumhof, The macroeconomics of central bank issued digital currencies. It evaluates the impact of CBDC on the economy. I believe it is a permanent deterministic shock. My problem is: since CBDC does not exist in the pre-CBDC economy, the quantity of CBDC and its interest rate should not exist. Then what should I do for the initial block? From the equations, if the quantity of CBDC is 0, then its interest rate would go to infinity because the quantity is at the denominator. So the steady state could not be solved.

From Barrdear and Kumhof’s paper, their IRF on real CBDC interest rate does not exist in the pre-CBDC economy. I was wondering does anyone know how they achieved this? Is this achieved by Dynare?

I asked Mr. Kumhof, one of the authors, about the paper. It turned out that they did not use Dynare, they used TROLL instead. The algorithm they are using is Newton stacking algorithm. I have no idea what it is. Will check. By the way, if anyone has a clue feel free to share.

The response you got is not really an answer. They are using a perfect foresight solver similar to the one used in Dynare. Given an initial and terminal condition, you need to solve a system of equations. But your problem is to find out what the initial condition was.

Hello, I have been studying this paper recently, but I have been unable to write the code. If possible, could you please share the code you copied?Thank you for your help

Hi, Jaxx.

I am also trying to replicate the paper lately, and I think I did for the model block.

However, it seems like without the initval block, the model will not find the steady-state.

If you have any clue on the initial condition, it would be much appreciated if you could share it with us.