estimation(datafile=estdata,mode_compute=6, presample=4,

prefilter=0,mh_replic=2000, mh_nblocks=5,mh_jscale=0.40,mh_drop=0.2, diffuse_filter, bayesian_irf,irf=40,conf_sig=0.9)y c i w l u pi r;

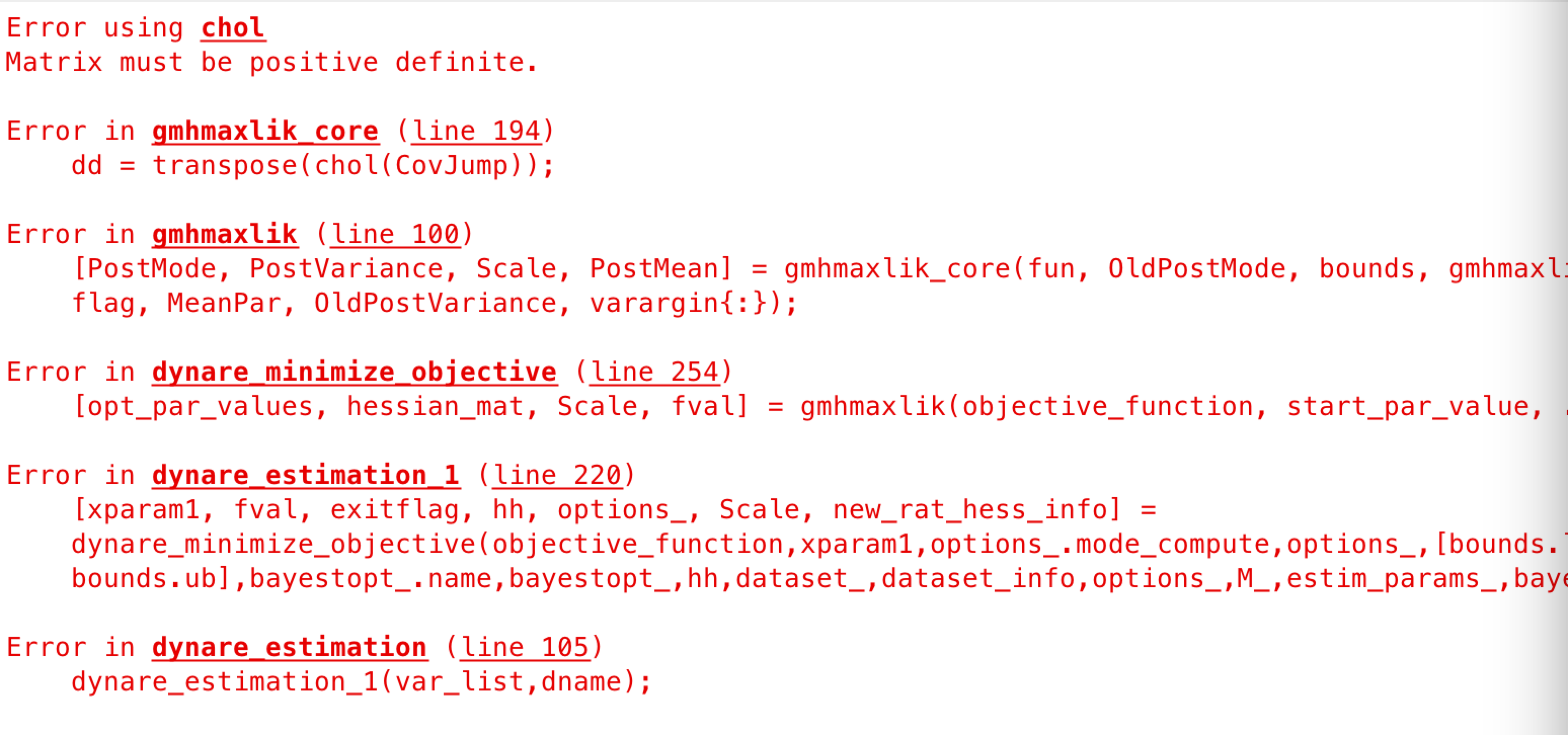

Your parameter zeta_inv is not identified, because you are not handling parameter dependence correctly. Search the forum on this.

Your prior is weird:

Prior distribution for parameter theta has unbounded density!

Prior distribution for parameter gammap has unbounded density!

Prior distribution for parameter gammap has two modes!

Prior distribution for parameter gammaw has unbounded density!

Prior distribution for parameter rho_a has unbounded density!

Prior distribution for parameter rho_b has unbounded density!

Prior distribution for parameter rho_g has unbounded density!

Prior distribution for parameter rho_i has unbounded density!

Prior distribution for parameter rho_pi has unbounded density!

You are trying to match non-zero mean data to zero mean variables in the model. That will cause issues, particularly combined with your prior that already pushes the AR processes to a unit root.